Key takeaway: Securing a safe mortgage requires verifying a broker’s Australian Credit Licence and demanding full transparency on commissions. Under the strict Best Interests Duty, professionals must prioritize borrower needs over their own financial incentives. Identifying red flags like pressure tactics, vague fees, or limited lender panels prevents costly long-term mistakes and ensures access to truly suitable loan products.

Common mortgage broker red flags to watch for:

- Can’t or won’t produce their ASIC Credit Licence or credit representative number

- Recommends one lender before asking about your income, goals or situation

- Vague or evasive when asked how their commission is calculated

- Skips a proper fact-find on your income, expenses, debts and plans

- Pressures you to sign quickly or skip reading the fine print

- Won’t provide a written comparison of at least two loan options

- Goes quiet after settlement instead of offering an annual review

Entrusting your financial future to an incompetent advisor is a nightmare scenario, yet spotting common mortgage broker red flags Australia early is the only way to protect your home ownership dreams.

This guide cuts through the industry noise to reveal the subtle warning signs of bad practice, from vague fee structures to pressure tactics that prioritize commissions over your specific needs.

You will walk away with a concrete verification checklist that empowers you to distinguish a genuine expert from a risky operator before signing a single document.

- Why Spotting a Bad Broker Matters in Australia

- Red Flags Around Legitimacy and Incentives

- Process, Product, and Communication Warning Signs

- The Ultimate Test: Questions to Ask and Documents to Expect

- What to Do If You’ve Hired a Bad Broker

Why Spotting a Bad Broker Matters in Australia

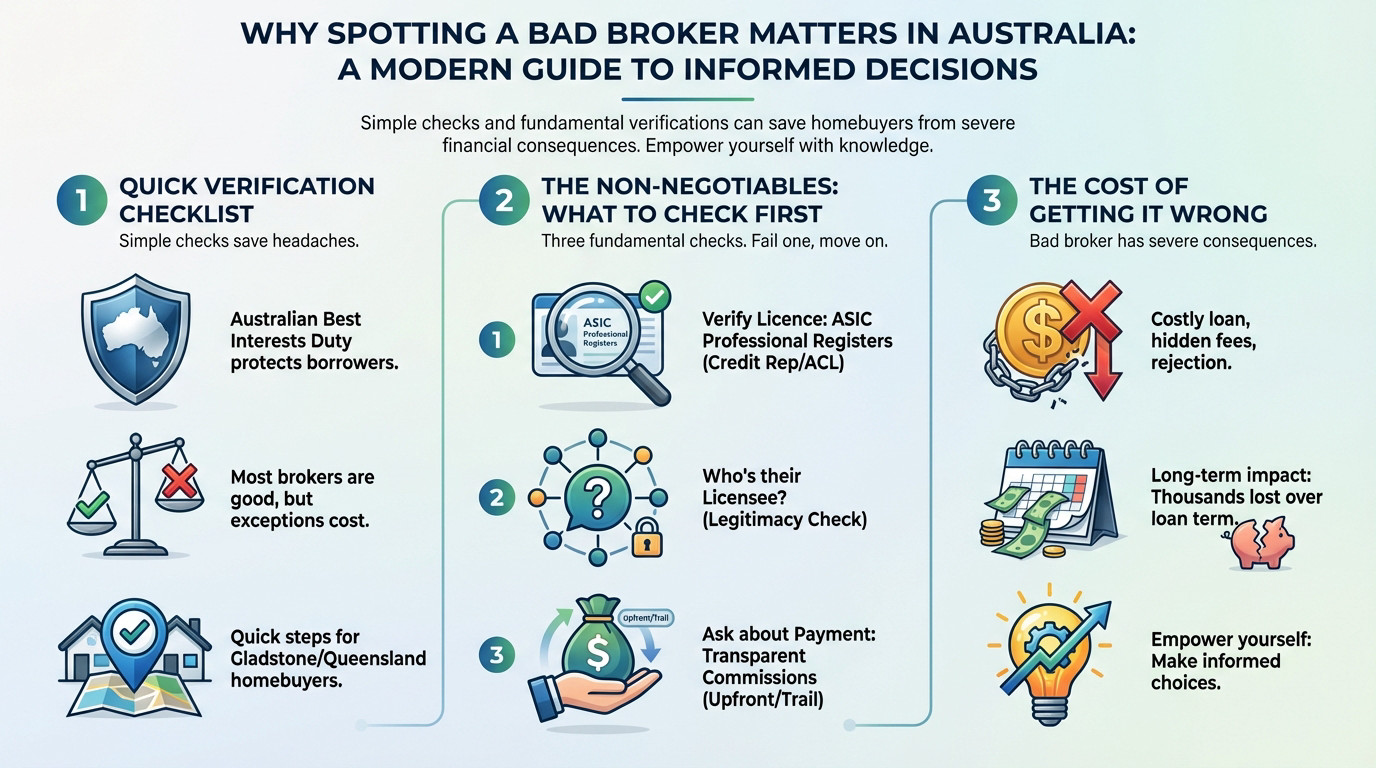

Your Quick Verification Checklist

Before booking that coffee, a few checks save massive headaches. Australia’s Best Interests Duty exists to protect you, but you must verify it applies. These mortgage broker red flags Australia warnings are vital.

Look, most brokers are legends who save you money. We are just hunting the few bad apples that cost you a fortune.

Think of this list as your primary filter. It only takes five minutes. It is the absolute first line of defense for any home buyer in Gladstone or across Queensland. Don’t skip it.

The Non-Negotiables: What to Check First

Here are three fundamental checkpoints you cannot ignore. If a broker fails even one of these tests, walk away immediately. It is simply not worth the risk to your financial future.

- Verify their licence: Check the broker’s name on the ASIC Professional Registers Search. They must be listed as a credit representative or hold an Australian Credit Licence (ACL).

- Understand who they work for: Ask “Who is your credit licensee?” This tells you which larger group they operate under and ensures their authorisations are legitimate.

- Ask how they get paid: A good broker will transparently explain their commissions (upfront and trail). This is standard practice, not a secret.

The Cost of Getting It Wrong

Picking the wrong broker isn’t just about enduring bad service. It often translates to a more expensive loan, nasty hidden fees, or a rejected application. You might even end up with a black mark on your credit file.

The consequences linger for years after the paperwork is signed. The wrong financial product can easily drain tens of thousands of dollars from your pocket over the loan’s life.

My goal is simple: giving you the tools to make a smart choice, whether you are a first home buyer in Gladstone or a seasoned investor.

Red Flags Around Legitimacy and Incentives

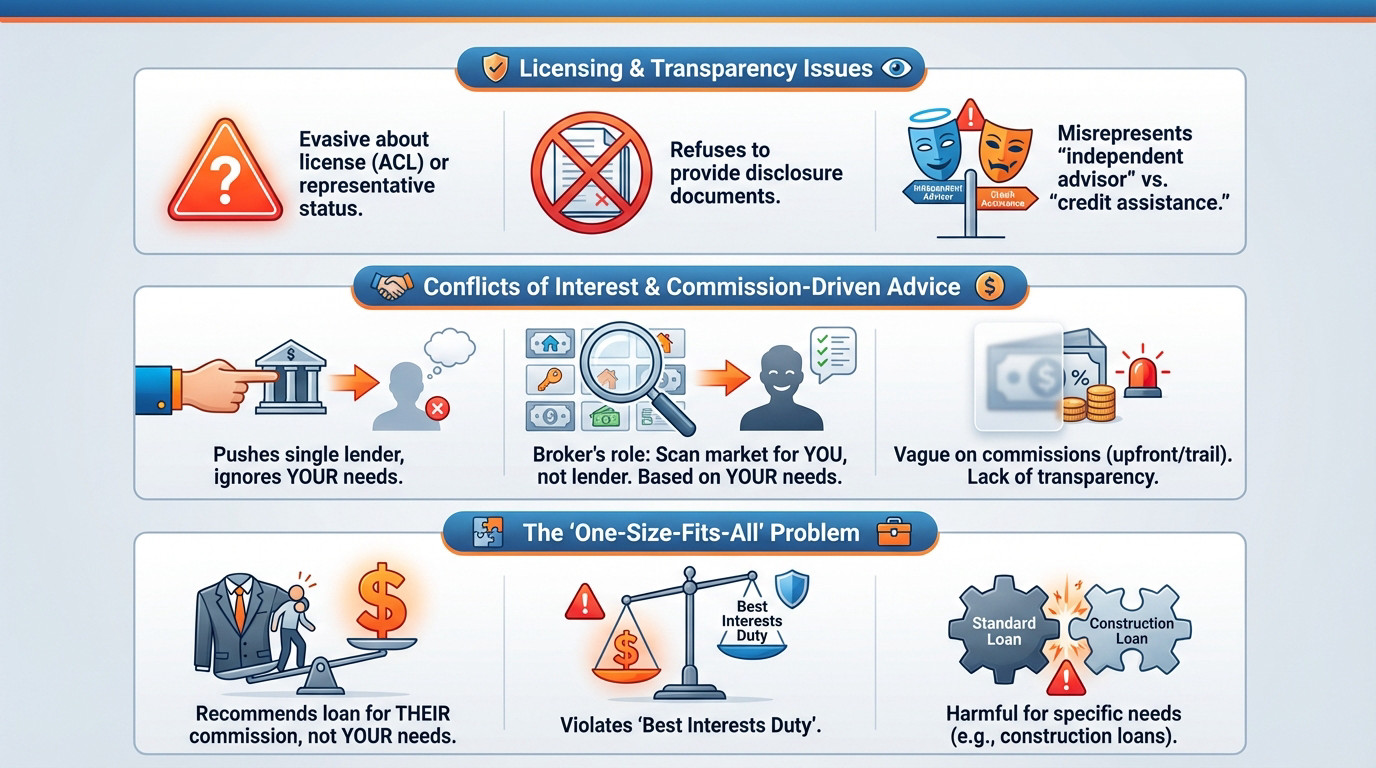

Licensing and Transparency Issues

A legitimate broker wears their credentials like a badge of honour. If they get shifty when you ask for their Australian Credit Licence (ACL) number or representative details, that is a huge red flag.

Never trust a broker who refuses to hand over disclosure documents upfront. ASIC mandates these papers so you actually understand the service you’re getting—hiding them is a major compliance breach.

Watch out for anyone claiming to be an “independent adviser” without clarifying they provide “credit assistance.” Under Australian law, these are distinct roles, and blurring the lines is often a deliberate tactic to confuse you about their obligations.

Conflicts of Interest and Commission-Driven Advice

If a broker shoves a single lender at you before even asking about your finances, run. They are acting like a bank branch in disguise, completely ignoring the vital difference between banks vs mortgage brokers.

A broker’s job is to scan the market for you, not for the lender. Their recommendation should be based on your needs, not their preferred sales channel.

Another warning sign is an inability to explain how they get paid. If they are vague about upfront and trail commissions, that lack of transparency is unacceptable.

The ‘One-Size-Fits-All’ Problem

Be wary of brokers recommending a loan type that bumps up their commission but doesn’t fit your life. For instance, pushing a massive credit facility you don’t actually need just to inflate the loan size.

This behavior goes directly against their Best Interests Duty. Remember, their legal role is to engineer the solution that fits you best, not the one that pads their wallet the most.

This lazy approach is dangerous for borrowers with specific needs, especially those looking for construction loans or navigating complex income streams.

Process, Product, and Communication Warning Signs

Beyond licensing and money, how a broker operates day-to-day reveals their true colors. Here are the warning signs related to their process, product choices, and communication style.

Sloppy Process and Lack of Competence

A major red flag is the lack of a structured fact-find. If they don’t ask detailed questions about your income, expenses, debts, and future plans, they can’t properly assess your situation. You are flying blind. This is dangerous territory.

Be wary of vague estimates and the classic “she’ll be right” attitude. A good broker runs specific checks against lender policies to assess your borrowing power accurately. Guesswork costs you money.

If they only talk interest rates and ignore fees, loan features, and overall suitability, they are doing half the job. The cheapest rate often hides the highest cost. Look deeper.

Poor Product Recommendations

A decent broker must explain why the recommended loan beats at least two credible alternatives. Otherwise, how do you know it is truly the best for you? Demand a comparison.

Vague claims like “this lender is easiest” or promises of “guaranteed approval” are signs of amateurism or dishonesty. No approval is ever 100% guaranteed until the letter arrives. Walk away fast.

If they push you into a fixed term without explaining break costs or discourage an offset account, watch out. It might be laziness, not because it fits your best interests. You deserve a strategy. Don’t settle for less.

Bad Communication and Pressure Tactics

Any broker who tells you to “sign today before the deal disappears” or “don’t worry about reading the fine print” is using pressure tactics, not providing advice.

This behavior is unacceptable. It signals a desperate salesperson.

Radio silence is another bad sign. A broker must be proactive with communication, especially when deadlines are tight. You should always know exactly where your file stands.

If they get defensive when you ask about their commission or lender panel, they have something to hide. Transparency should be the standard for any local mortgage expert. Trust your gut here.

The Ultimate Test: Questions to Ask and Documents to Expect

Knowing the theory is one thing, but you need to see how a broker reacts under pressure. Here are the specific questions to ask and the documents you must demand to ensure they are legitimate.

Questions That Expose Red Flags Fast

Arm yourself with these specific questions during your first meeting to spot mortgage broker red flags Australia-wide. If they dodge the answer or get defensive, that is your cue to walk away immediately.

- Who is your credit licensee and ASIC register details?

- How many lenders are on your panel, and do you have any volume-based incentives

- How will you be paid for this loan, specifically? Can you break down the upfront and trail commissions?

- What are the top 3 lenders you’re considering for me and why?

- Can you list the top 5 reasons this recommended loan is in my best interests and explain the trade-offs?

- What are all the fees involved—now, during the loan, and on exit?

What a Good Broker’s Paperwork Looks Like

A professional process always ends with clear, written documentation. A trustworthy broker never relies on verbal conversations alone; they back up every recommendation with hard evidence you can review.

| Key Documents a Good Broker Provides | Why It Matters |

|---|---|

| Written Comparison & Rationale | This is the proof that they’ve acted in your best interests. It should compare at least 2-3 loan options and clearly state why the recommended product was chosen for your specific situation. |

| Commission Disclosure | A formal document showing exactly how much the broker will be paid by the lender. Full transparency is required by law. |

| Servicing Assessment Summary | Shows the income, expenses, and liability figures used to calculate your borrowing capacity. This confirms they’ve used accurate information and haven’t suggested you “fudge the numbers”. |

After-Settlement and Refinancing Red Flags

The work of a quality broker does not stop at the signature. If they disappear immediately after the loan settles, that is a bad sign; they should offer annual reviews.

Méfiez-vous du “refinance churn.” This happens when a broker pushes you to refinance frequently just to generate new commissions, without providing any real net benefit to your financial situation.

A good broker should be able to clearly articulate the advantage of home loan refinancing. It goes beyond a simple “lower rate” and must account for all associated costs and structure.

What to Do If You’ve Hired a Bad Broker

So, you are reading this and realizing you might have spotted some mortgage broker red flags Australia warnings in your own situation. Don’t panic; you have options to fix this before it costs you money.

Changing Course Mid-Application

If you have not signed a loan offer yet, you can absolutely switch brokers. It is your fundamental right as a consumer to walk away from bad service.

Send a simple email to your current broker stating you are terminating their services immediately. Make sure you collect every document you previously sent them; handing this complete file to your new broker saves days of work.

Speed matters here. If you have a finance date looming on a contract, do not wait another hour to act.

Reporting Unethical Behaviour

If a broker acts illegally or unethically, you need to report it. Speaking up stops them from hurting other families in the Gladstone property market.

Start by contacting the broker’s internal dispute resolution team. Their details must be listed in the Credit Guide they gave you at the start.

If that fails, lodge a complaint with the Australian Financial Complaints Authority (AFCA). For serious issues like fraudulently inflating income, contact ASIC directly.

When a Broker Is Worth It vs. Going Direct

A skilled broker is invaluable when life isn’t cookie-cutter. If you are self-employed, have tight servicing, or need to juggle specific lender policies, do not go it alone.

- Go with a broker if: You have complex income, are self-employed, need to compare multiple lenders, or are a first-time buyer needing guidance. A good broker, like the team you can learn about at AJ Home Loans Gladstone, adds immense value here.

- Going direct can work if: You have a simple PAYG income, a large deposit, you already know exactly which lender and product you want, and you are confident in negotiating yourself.

Securing the right home loan requires a partner you can trust. By staying vigilant against these red flags, you protect your financial future. If you are looking for transparent, expert guidance in Queensland, our team is ready to support your property journey.

Book an appointment in Gladstone

FAQ

How can I officially verify if a mortgage broker is licensed in Australia?

You can verify a broker’s credentials by searching their name on the ASIC Professional Registers. By law, they must either hold their own Australian Credit Licence (ACL) or be listed as an authorised credit representative of a licensee.

If a broker cannot provide their licence number or does not appear in the ASIC registry, do not proceed. Operating without proper authorisation is illegal and a definitive red flag regarding their legitimacy.

What are the biggest red flags to look out for during my first meeting?

Be wary of brokers who use high-pressure tactics, such as urging you to sign immediately before a “deal expires.” A professional broker will encourage you to take the time to understand the product. Another major warning sign is if they push a single lender without offering a comparison or explaining why it suits your specific financial situation.

Additionally, pay attention to their communication style. If they are disorganised, lose documents, or fail to ask detailed questions about your expenses and future goals, they are likely not conducting a thorough assessment of your needs.

Do mortgage brokers charge hidden fees, and how do they actually get paid?

Most brokers in Australia are paid commissions (upfront and trail) by the lender, not the borrower. However, they are legally required to provide a document disclosing exactly how much commission they will receive for your loan. If they are vague about this, it is a serious concern.

While some brokers may charge a fee for service, this must be quoted upfront in their Credit Guide. If you encounter unexpected “admin fees” or costs that were not discussed early in the process, ask for a written explanation immediately.

What specific documents must a broker provide to prove they are acting in my best interests?

A reputable broker must provide a Credit Proposal or a Statement of Credit Assistance. This document outlines the loan they are recommending, the fees involved, and the specific reasons why this product was chosen over others to meet your objectives.

They should also provide a written comparison of at least two or three different loan options. This documentation serves as proof that they have followed the Best Interests Duty required by Australian law.

What should I do if I suspect my broker has given me bad advice or acted unethically?

If you believe a broker has acted poorly, first contact their internal dispute resolution team; their contact details should be in the Credit Guide they provided. If the issue is not resolved, you can lodge a complaint with the Australian Financial Complaints Authority (AFCA).

AFCA provides a free, independent dispute resolution service for consumers. For serious misconduct, such as fraud or suggesting you falsify application documents, you should also report the broker to ASIC.