Key takeaway: the choice between a broker and DIY relies on risk management, not just interest rates. Brokers offer access to over 70 lenders and legal protection under the Best Interests Duty, vital for complex incomes. While DIY offers control, it suits only simple profiles, as mismanagement risks credit score damage through multiple hard inquiries.

Are you unknowingly exposing your financial future to higher interest rates and potential credit damage by managing your property loan application alone?

The strategic choice between a dedicated mortgage broker vs do it yourself home loan Australia determines whether you access leverage for better terms or settle for standard retail banking offers.

We expose the hidden lender policies and specific negotiation mechanics that prove which option actually minimizes your risk and maximizes your long-term savings in the current market.

- Broker vs DIY: The Real Difference Is More Than Just the Rate

- When a Mortgage Broker Is Your Best Bet

- When the DIY Home Loan Path Can Work

- How to Make the Right Choice for You

Broker vs DIY: The Real Difference Is More Than Just the Rate

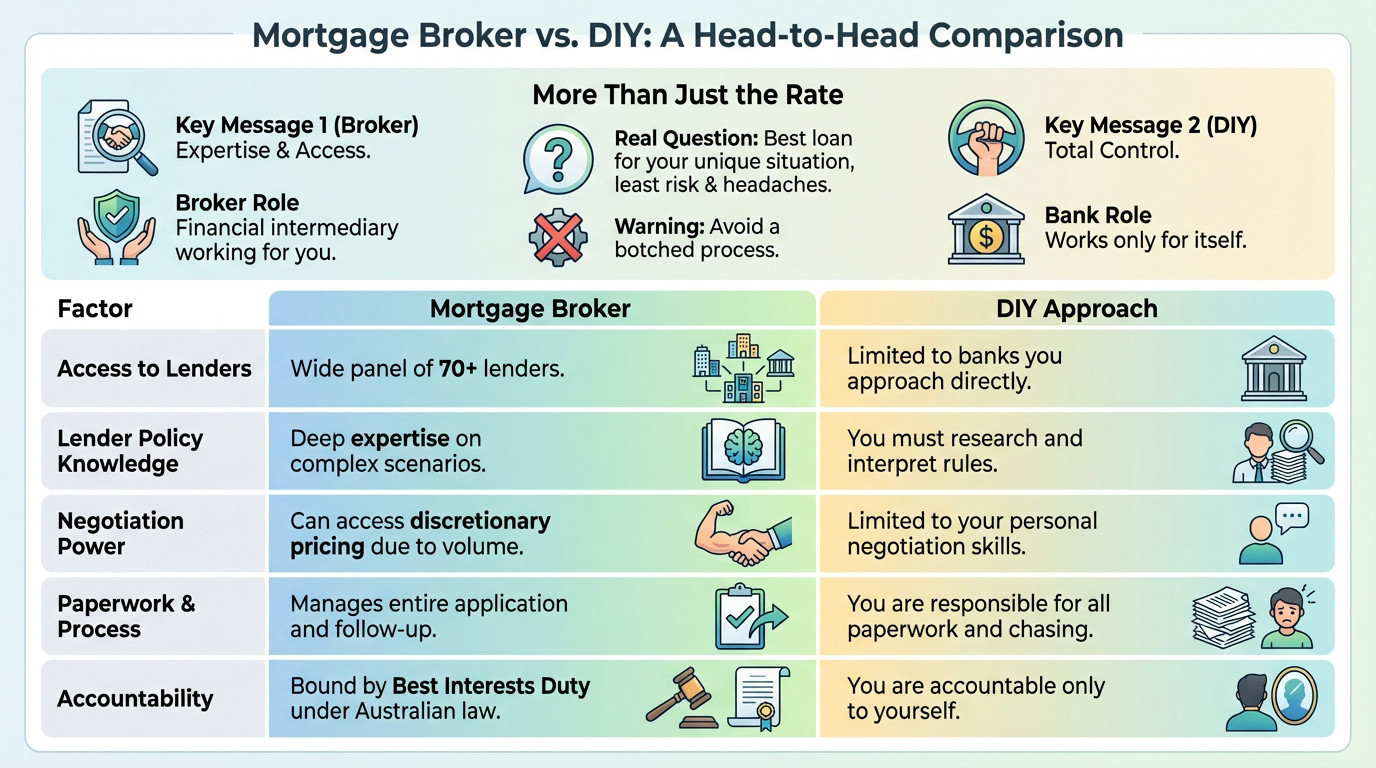

What You’re Really Choosing Between

You aren’t just picking a rate; you are choosing between expert access and the solitude of a DIY approach. A mortgage broker acts as an intermediary working for you, whereas a bank officer only works for the bank.

The real question is: which path secures the best loan without the migraine? The true enemy isn’t the bank; it is a sloppy process.

Access, Policy Knowledge, and Negotiation Power

Let’s look at the hard facts. The table below breaks down exactly where the leverage shifts between handling it yourself and using a professional.

| Factor | Mortgage Broker | DIY Approach |

|---|---|---|

| Access to Lenders | Wide panel of 70+ lenders | Limited to banks you approach directly |

| Lender Policy Knowledge | Deep expertise on which lender accepts complex scenarios | You must research and interpret each lender’s rules |

| Negotiation Power | Can often access discretionary pricing due to volume | Limited to your personal negotiation skills |

| Paperwork & Process | Manages the entire application and follow-up for you | You are responsible for all paperwork and chasing the bank |

| Accountability | Bound by Best Interests Duty under Australian law | You are accountable only to yourself |

A sharp broker knows which lender accepts self-employed income or probation periods. A bank’s website won’t reveal these policy secrets; you need that inside intel.

Simply understanding the difference between banks and brokers prevents bad loans. Banks sell their own products, while brokers shop the market to fit your needs.

When a Mortgage Broker Is Your Best Bet

Now that the basics are clear, let’s look at specific situations where a broker’s expertise becomes a major asset.

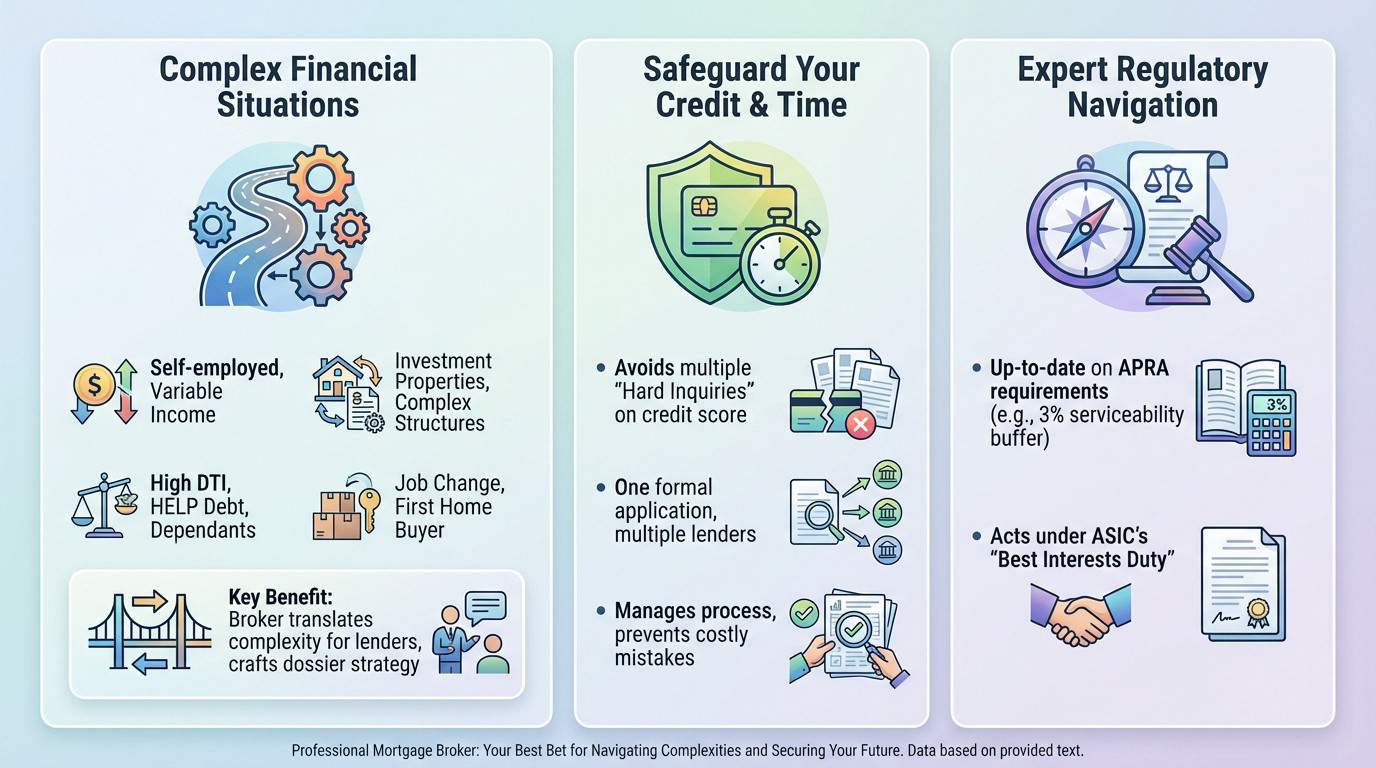

If Your Financial Life Isn’t a Straight Line

Banks love boxes. In the mortgage broker vs do it yourself home loan in Australia debate, a broker wins if your life is complex. You need an expert in your corner.

If any of these points apply to you, expert help is vital for approval:

- You’re self-employed, a contractor, or rely on variable income like commissions.

- You’re eyeing investment properties, have complex structures, or plan debt recycling.

- Your borrowing power is tight due to a high debt-to-income (DTI) ratio or HELP debt.

- You’ve changed jobs or are a first home buyer in Gladstone needing guidance.

A broker acts as your translator, presenting your story so lenders actually listen. It is about loan strategy, not just raw numbers.

Protecting Your Credit Score and Saving Time

Here is the blind spot: every formal DIY application leaves a “hard inquiry” on your file. Too many can wreck your rating.

We stop this damage. A broker sounds out multiple lenders with one file, protecting your credit score.

A good broker doesn’t just find you a loan; they manage the entire process to protect your financial standing and prevent costly mistakes before they happen.

Navigating the Rules: APRA and ASIC

Rules change fast. A broker navigates APRA requirements, like the 3% serviceability buffer, ensuring you don’t hit a wall.

Legally, we must act in your favour under the Best Interests Duty. That is an ASIC protection you won’t get at a bank branch.

When the DIY Home Loan Path Can Work

But a broker isn’t always the only solution. In very specific situations, managing your loan yourself can be a viable option.

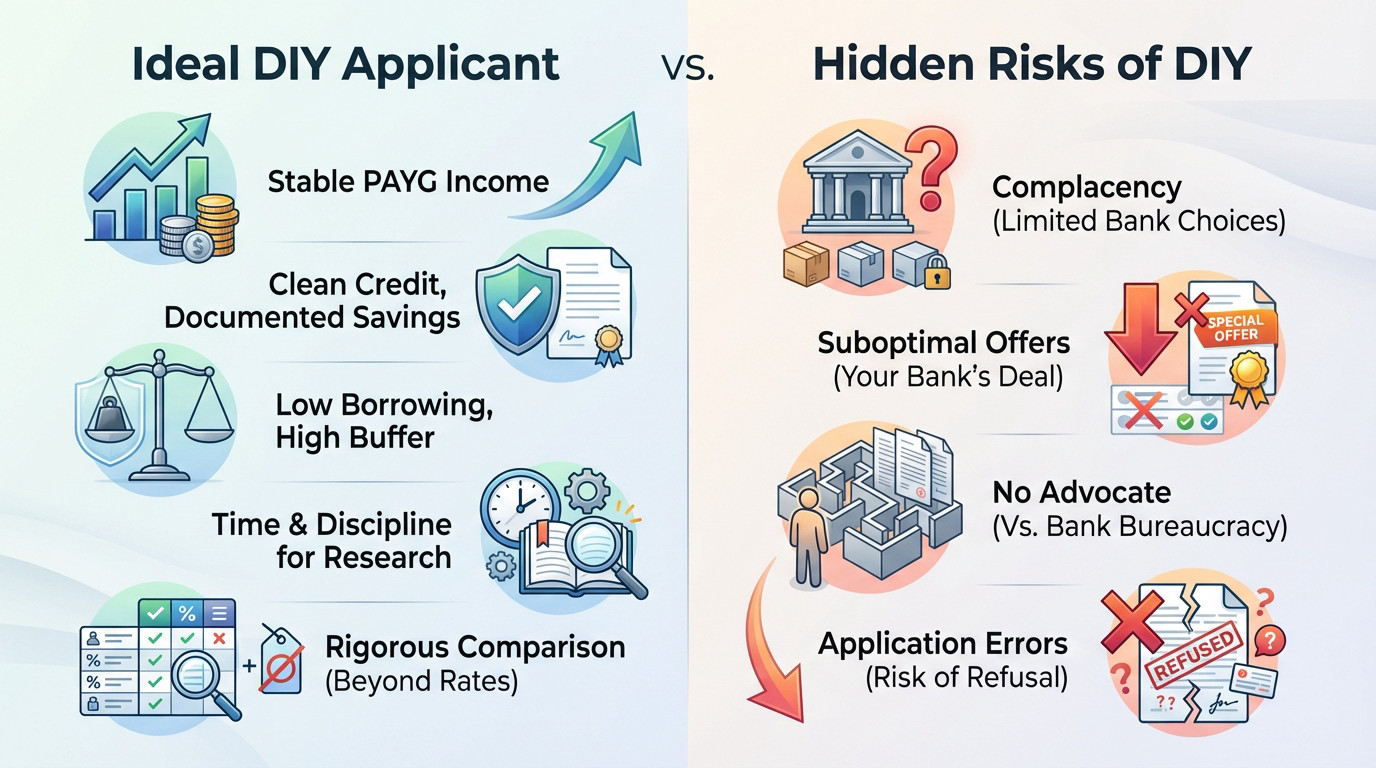

The Profile of a Successful DIY Applicant

Let’s be honest: going solo works, but only if your finances are vanilla and you are incredibly disciplined. It is not for everyone.

If you tick every box below, you might safely navigate the mortgage broker vs do it yourself home loan Australia debate without help.

- You have a stable PAYG income with a long history at your employer.

- credit history is clean and your savings are clearly documented.

- You are not borrowing at maximum capacity and have a significant buffer.

- You have the time and discipline to compare multiple lenders properly, read fine print, and negotiate.

Success demands rigor. You cannot just pick the lowest rate on a comparison site; you must personally analyze fees, features, and policies.

The Hidden Risks of Going It Alone

The biggest danger isn’t rejection, but complacency. Most DIY borrowers stop searching after checking just one or two banks.

Without an expert pushing you, it is easy to accept your current bank’s offer, which is rarely the most competitive choice.

You also have nobody to fight your corner against the bank’s bureaucracy if the process stalls.

Even simple scenarios make securing a formal home loan pre-approval delicate. One DIY application error can trigger an avoidable decline.

How to Make the Right Choice for You

So, how do you decide? It comes down to understanding motivations and knowing exactly what to demand, whether you choose a broker or the DIY route.

Understanding the Money Trail: How Brokers Are Paid

Let’s be real about the “free” service myth. Brokers get paid by the lender through an upfront commission and a recurring trail commission. It’s a business model, not charity.

However, the law is on your side. Under the Best Interests Duty, a broker must prove why a specific loan suits you better than others. If they can’t explain the math behind their choice, walk away immediately.

What a ‘Good’ Process Looks Like (Your Non-Negotiable Standards)

Whether tackling a mortgage broker vs do it yourself home loan Australia comparison, success relies entirely on process quality. Here is the standard you must demand.

- If using a broker: They ask detailed questions, explain their pay, present 2-3 options with trade-offs, and put their recommendation in writing explaining the benefit.

- If going DIY: You shortlist lenders based on policy fit first, compare identical loan structures, and actively negotiate for discretionary pricing—never just accept the advertised rate.

A good broker must be able to articulate precisely why their recommendation is in your best interests and be willing to put that rationale in writing for you.

Government guides like MoneySmart provide practical checklists to hold your professional accountable. Use them to ensure you aren’t getting stitched up.

Common Failure Modes to Avoid

A “bad broker” is dangerous because they take the path of least resistance. They steer you toward the lender with the easiest paperwork or highest commission, ignoring better options.

A “bad DIY” approach is often worse. Borrowers who do a lazy comparison and accept the first rate from their current bank end up overpaying thousands of dollars over the loan term.

Ultimately, choosing between a mortgage broker and a DIY approach depends on your financial complexity and available time. While going solo offers control, a broker ensures expert protection and wider market access. Don’t leave your financial future to chance. Book an appointment in Gladstone today to secure the right loan strategy.

FAQ

Do mortgage brokers actually get better rates than going direct?

Often, yes. Brokers have access to “discretionary pricing” and wholesale rates that are not advertised to the general public. Because they bring volume to lenders, they can leverage this to negotiate interest rate discounts that an individual DIY applicant might struggle to secure alone.

However, a broker’s value isn’t just the rate; it is matching that rate to a policy that accepts your income type. A low advertised rate is useless if the bank rejects your application due to strict lending criteria.

How much does a mortgage broker cost me in Australia?

For most residential home loans, a mortgage broker’s service is free to you. They are compensated by the lender through an upfront commission and a trailing commission over the life of the loan. This structure applies to the vast majority of standard borrowers.

Fees may only apply in specific complex situations, such as commercial lending or short-term loans. A reputable broker will always disclose their commission structure and any potential costs in their Credit Guide before you proceed.

Is it risky to apply for a home loan myself (DIY)?

The primary risk of a DIY approach is damaging your credit score through “shopping around” with formal applications. Every time you apply directly to a bank and get rejected—or even just assessed—it leaves a “hard inquiry” on your credit file. Too many of these can make you look risky to future lenders.

Furthermore, you risk rejection by not understanding the fine print of a lender’s credit policy. A broker mitigates this by identifying which lenders accept your specific financial profile before a formal application is ever lodged.

Why trust a broker if they are paid a commission by the bank?

In Australia, mortgage brokers are bound by the Best Interests Duty (BID), a law monitored by ASIC. This legislation legally requires them to prioritize your interests above their own commissions or a specific lender’s preferences. They must prove why a recommended loan is right for you.

Bank employees, by contrast, are not bound by BID. They are sales staff for their specific institution and have no legal obligation to tell you if a competitor offers a cheaper or better product.