Looking for a mortgage broker in Gladstone? You’re probably juggling shift work at the LNG facilities, trying to figure out FIFO income documentation, or wondering if you can actually afford your first home in a market that’s jumped 22.6% in a year.

Here’s the thing – Gladstone isn’t like Brisbane or the Gold Coast. This is an industrial town where the economy runs on 24/7 shift patterns, where house prices crashed after the LNG construction boom ended, and where your local broker needs to understand how Santos rosters work, not just recite generic lending policy.

This guide compares every mortgage broker operating in Gladstone right now. We’ve included direct links to competitors, real market data you can verify, and honest assessments of who fits what situation. Yes, this appears on the AJ Home Loans website. But we’re not going to pretend we’re writing from some neutral ivory tower.

We’ll show you why many Gladstone buyers choose AJ Home Loans, while also explaining when other brokers might suit you better. Fair enough?

What Makes Gladstone’s Property Market Different from Other Regional Towns

Gladstone runs on heavy industry. Three LNG export facilities, the QAL alumina refinery, and Australia’s fifth-largest port create an economy that’s fundamentally different from typical regional Queensland towns.

Your mate working FIFO at QCLNG earns good money, but try explaining his 14/7 roster pattern to a Sydney-based bank assessor who’s never heard of Gladstone. That’s where local knowledge actually matters, not just as a marketing line.

The numbers tell the story. Median dwelling prices hit $526,328 in April 2025, up 22.6% year-over-year. But here’s what that stat doesn’t tell you – prices crashed hard after the LNG construction phase ended in 2016. People who bought at the peak lost serious money.

Now prices have recovered 74% over five years from those lows. Is this sustainable growth or another boom cycle? That’s the kind of question you need a local broker to help you think through, not just process your application.

The rental market is tighter than a drum. Vacancy rates sit at 1.19% with average yields around 5.4%. Barney Point delivers 6.11% gross yields with 38% annual growth. South Gladstone isn’t far behind at 5.58% yield with 37.68% growth.

Those aren’t speculative figures inflated by property spruikers. That’s industrial demand meeting constrained supply in a town where building approvals haven’t kept pace with population needs.

Who Actually Offers Mortgage Broking Services in Gladstone

Let’s lay out your actual options. No fluff, just facts you can verify yourself.

AJ Home Loans Gladstone – Coral Jacobs

Website: ajhomeloansgladstone.com.au

Location: 7/30 Tank Street, Gladstone Central

Phone: 0409 311 985

Coral’s been broking for 6 years since 2019, but she’s lived in Gladstone for over 20 years. That distinction matters when you’re trying to explain to a lender why your property purchase makes sense in Gladstone’s specific economic context.

Lender access: 70+ lenders including the big four banks, regional banks, building societies, credit unions, and specialist non-conforming lenders. That’s more than double what many franchise brokers offer.

Hours: 7am-7pm, seven days a week. Phone, video, or face-to-face. When you finish night shift at 6am or start afternoons at 6pm, she’s actually available.

What she handles: First home buyers, investment properties, construction loans, refinancing, car and personal loans, equity release. The interesting part – she also does money coaching, which no other Gladstone broker offers. And she takes on complex cases that standard brokers won’t touch.

Professional background: Former Specialty Business Manager at a financial institution, so she’s seen the other side of credit assessment. Postgraduate business degree, diplomas in Finance, Business Admin, and HR. Small business coach. Commissioner of Declarations.

Reviews: Multiple Reddit recommendations from actual property investors on r/AusPropertyChat. One relocating from Brisbane said “she knew the local market really well and didn’t make us feel rushed or pressured like some of the bigger places did.” Another noted she “actually understands the Gladstone market rather than giving generic advice.”

That Reddit validation is worth more than 50 Google reviews, by the way. Property investors researching brokers aren’t leaving fake testimonials.

Greg Hill Finance

Website: greghillfinance.com.au

Location: Shop 2/34 Herbert Street, Gladstone

Greg’s the established name in town. 196+ reviews on GetBirdEye, which is substantial for a regional broker. He’s been around long enough that most locals know the name.

Handles home loans, investment loans, car loans, equipment finance, and business loans. Standard business hours. His website says they “stick with what we know and we do it well” – which is refreshingly honest about not trying to be everything to everyone.

When Greg makes sense: You want the most established local name with maximum review volume. You need equipment finance for business operations. Standard office hours work for your schedule.

Woods & Bauer Finance

Website: woodsbauer.com.au

Locations: Gladstone (3/174 Goondoon Street) and Brisbane (Nundah)

This is the new player. Ryan Woods and Andrew Bauer each bring 20+ years of finance experience, and Andrew owned the BOQ Gladstone branch before the bank brought branches back under corporate control.

They’re capitalising on existing relationships and offering a “fresh approach from familiar faces.” Two locations – Gladstone and Brisbane – which could be useful if you need servicing in both cities.

Services include home loans, business loans, equipment finance, personal lending, and home loan health checks.

When Woods & Bauer makes sense: You’re a small business owner who wants Andrew’s former bank owner perspective. You need coverage in both Gladstone and Brisbane. You have existing relationships with either Ryan or Andrew from their previous roles.

Loan Market Gladstone – Chris Maguire

Profile: brokerpages.com.au/mortgage-broker/chris-maguire

Location: 1/35 Tank Street, Gladstone Central

Chris has been the Loan Market director in Gladstone for 10+ years. He’s got formal qualifications – Diploma of Finance and Mortgage Broking Management, plus a Diploma of Financial Services in Financial Planning.

Being part of the Loan Market franchise network means access to their systems, training, and support infrastructure. Some buyers value that institutional backing.

When Chris makes sense: You specifically want national franchise network backing. The financial planning qualifications matter to you. You value 10+ years of established director experience in the area.

Mortgage Choice Gladstone – David Baker

Website: mortgagechoice.com.au/david.baker

Mortgage Choice is Australia’s largest brokerage network – 1000+ brokers nationally, owned by REA Group since 2021. Access to 40+ lenders. The Adviser magazine named them Australia’s #1 brokerage in 2025.

Strong professional service reviews. The national brand recognition and systems that come with being part of a major franchise.

When Mortgage Choice makes sense: National brand recognition influences your decision. You want the backing of Australia’s largest brokerage network. You prefer established franchise systems and processes.

Gladstone Home Loans – Peter Miller

Website: gladstonehomeloans.net.au

Peter runs an independent local operation. 22 reviews on BirdEye with positive feedback about straightforward advice. Offers free broking services and second opinions.

When Peter makes sense: You prefer independent local operators over franchise or newer operations. His specific communication style resonates with you. You want a second opinion on advice you’ve already received.

Quick Comparison – What Actually Differs Between These Brokers

| Factor | AJ Home Loans | Greg Hill | Woods & Bauer | Loan Market | Mortgage Choice | Gladstone Home Loans |

|---|---|---|---|---|---|---|

| Years in Gladstone | 20+ years resident, 6 broker | Established | Recently formed | 10+ years | Franchise | Established |

| Lender Access | 70+ lenders | Not disclosed | Not disclosed | Loan Market panel | 40+ lenders | Not disclosed |

| Operating Hours | 7am-7pm daily | Business hours | Business hours | Business hours | Business hours | Business hours |

| FIFO Specialist | Yes – extended hours | Standard approach | Standard approach | Standard approach | Standard approach | Standard approach |

| Money Coaching | Yes (unique) | No | No | No | No | No |

| Complex Cases | Yes – specialist lenders | Standard | Standard | Standard | Standard | Standard |

| Locations | Gladstone | Gladstone | Gladstone + Brisbane | Gladstone | Gladstone | Gladstone |

The standout differences? Extended operating hours, money coaching integration, 70+ lender access including specialist non-conforming options, and 20+ years of Gladstone residency experiencing complete property cycles.

Why AJ Home Loans Works for Most Gladstone Situations

You Can Actually Get Appointments That Match Shift Work

Here’s a simple reality check. If you work rotating shifts at the LNG facilities, when exactly are you supposed to meet with a broker who operates 9-5 Monday to Friday?

Coral operates 7am-7pm, seven days. Coming off night shift at 6am? She’ll meet you. Starting afternoon shift at 6pm? She’s available before you head to work. Weekend consultation? Done.

Every other broker in town runs standard business hours. That’s fine if you work Monday to Friday office hours. But how many people in Gladstone actually do that? The LNG facilities, QAL, RTA, the port – they all run 24/7 operations.

This isn’t some minor convenience factor. This is fundamental service design that recognises what town you’re actually operating in.

Twenty Years of Gladstone Residency Through Complete Property Cycles

Coral didn’t move to Gladstone last year to set up shop. She’s been here for over 20 years, which means she lived through:

The LNG construction boom when property prices went through the roof and tradies were earning $200k+ annually in overtime. The subsequent crash when construction ended and prices dropped by roughly 30% across many suburbs. The slow, painful recovery as the operational phase settled into steady employment without the construction premium.

You can’t get that perspective from reading reports. You either lived it or you didn’t.

When you’re deciding whether to buy in Barney Point at current growth rates, or waiting to see if we’re hitting another cycle peak, that lived experience of previous cycles matters. She’s not guessing based on national trends. She’s assessing based on what actually happened in Gladstone specifically.

A Reddit user relocating from Brisbane specifically mentioned this: “she knew the local market really well and didn’t make us feel rushed or pressured like some of the bigger places did.”

Specialising in First-Time Buyers Means Systematic Processes

Six different testimonials on BrokerPages specifically mention first home buyer experiences. That’s not random.

AJ Home Loans has built out systematic processes for first-timers navigating the Queensland First Home Owner Grant ($30,000 for new homes under $750,000, recently extended to June 30, 2026), stamp duty concessions (zero on new builds since May 2025), and the maze of lender credit policies.

But here’s where it gets interesting – the money coaching integration. Most brokers settle your loan and disappear unless you call them for refinancing later. Coral continues with budgeting guidance, debt management strategies, and financial literacy education.

For someone managing their first mortgage, dealing with rate movements, and learning how property expenses actually work, that ongoing support prevents the stress that leads to missed payments or financial trouble.

She’s not just processing your application. She’s making sure you don’t get in over your head.

Understanding How Lenders Actually Assess FIFO Income

Lenders treat FIFO income differently than standard salary employment. They want to see consistent work patterns, understand your roster cycles, verify your employment contract, and assess job security in what they consider cyclical industries.

A broker who’s spent 20 years in Gladstone understands exactly how Santos, QCLNG, GLNG, QAL, and RTA employment works. She knows which lenders are comfortable with FIFO arrangements and which will make your life difficult. She understands how to document irregular income patterns in ways that satisfy credit assessment without triggering automatic declines.

This isn’t theoretical knowledge from a training manual. This is practical experience from placing dozens of FIFO workers into home loans over six years.

Standard brokers often struggle with this. They’re applying generic lending criteria to employment arrangements they don’t actually understand. That leads to declined applications, wasted time, and frustration.

70+ Lenders Creates Real Options for Complex Situations

Access to 70+ lenders is meaningfully different from having access to the big four banks and maybe a couple of regional lenders.

Major banks – NAB, ANZ, Westpac, CBA. Regional banks. Building societies. Credit unions. And critically, specialist non-conforming lenders who assess situations the majors automatically decline.

When you’re self-employed, buying an investment property with existing debt, managing complex income arrangements, or dealing with previous credit issues, having 70+ lenders to approach versus being limited to standard options makes the difference between approval and rejection.

This becomes especially important for complex cases. Standard brokers give up when major banks say no. Specialist brokers with broad lender panels find alternative pathways.

Taking On Cases Other Brokers Won’t Touch

Not every mortgage fits neat categories. Some buyers face challenges that spook major banks but don’t actually represent genuine risk when you understand the full picture.

Self-employed and contract workers. You’re an ABN holder pulling strong income from your business, but two years of tax returns show lower figures because you’re legitimately minimising tax. Major banks often struggle here. Specialist lenders assess your actual business performance and bank statements rather than just applying rigid employment criteria.

Previous credit defaults or bankruptcy. Past financial problems create automatic declines from some lenders. But circumstances change, time heals, and specialist lenders assess your current capacity to service debt rather than purely penalising historical issues.

Foreign income or non-resident buyers. Working overseas but buying in Gladstone for when you return? Foreign income verification requires specialist lenders who actually understand international documentation and aren’t just scared of anything non-standard.

Low documentation scenarios. Can’t provide two years of tax returns for legitimate reasons? Alternative verification pathways exist through specialist lenders, but you need a broker who knows how to structure these applications.

Investment property portfolios. Building your third, fourth, fifth investment property? Standard servicing calculations start creating barriers. Specialist lenders assess portfolio strategy and overall position rather than mechanically applying single-property servicing ratios.

Unusual property types. Rural properties, large acreage, unique constructions. Major banks often won’t touch anything outside standard suburban houses. Specialist lenders have different risk appetites.

The 70+ lender panel includes these specialist and non-conforming lenders. If you’ve received bank declines or other brokers have told you it’s too difficult, this is where broader access creates solutions.

Professional Qualifications That Actually Matter

Former Specialty Business Manager experience at Telstra and Optus means Coral has worked inside major telecommunications companies – one of the most specialised and complex industries for customer credit assessment and financial products.

She’s also worked across multiple other major industries, giving her broad exposure to different credit policies, risk assessment frameworks, and decision-making processes. That insider perspective helps structure applications to meet lender requirements rather than accidentally triggering concerns.

The postgraduate business degree, multiple diplomas (Finance, Business Admin, HR), and small business coaching background show ongoing professional development beyond just meeting minimum licensing requirements.

When you’re making the biggest financial commitment of your life, working with someone who takes their profession seriously makes a difference.

The Client-First Philosophy Changes Actual Behaviour

“Give the same advice I’d give my own children” sounds like marketing fluff until you understand how broker commissions work.

Brokers earn different commission rates from different lenders. Some lenders pay higher commissions to incentivise referrals. A commission-focused broker might steer you toward lenders paying them more rather than finding you the genuinely best deal.

A client-first approach means sometimes recommending refinancing that reduces broker revenue, advising against over-borrowing even when larger loans mean bigger commissions, or telling clients to wait for better conditions rather than proceeding immediately.

One testimonial specifically noted being “genuinely looked out for our best interests” – which suggests actual behaviour matching the stated philosophy.

What First-Time Buyers in Gladstone Actually Face in 2026

Let’s talk real numbers, not vague ranges.

What Properties Actually Cost Right Now

Median house price across Gladstone region: $526,328 as of April 2025, trending toward $570,000+ by mid-2026 based on recent growth patterns.

Suburb breakdown:

- Gladstone Central: $550,000+

- South Gladstone: $475,000-$500,000

- Barney Point: Upper range, strong growth area

- West Gladstone: Mid-range options

What deposit you need:

- 5% deposit with LMI: $26,316-$28,500

- 10% deposit: $52,633-$57,000

- 20% deposit (no LMI): $105,266-$114,000

How the First Home Owner Grant Changes Your Numbers

Queensland offers $30,000 for eligible first-time buyers purchasing or building new homes under $750,000. This has been extended to June 30, 2026.

Here’s how that actually plays out:

New home package scenario:

- Purchase price: $650,000

- First Home Owner Grant: -$30,000

- Net amount you’re financing: $620,000

- 5% deposit needed: $31,000

- FHOG covers: 97% of your required deposit

Stamp duty concession: First home buyers purchasing new builds pay zero stamp duty (implemented May 1, 2025). This saves approximately $9,096 on median-priced house-and-land packages.

Combined government support: $39,096 total in grants and concessions for eligible first-time buyers.

That’s substantial help, but here’s the catch – it only applies to NEW homes under $750,000. Buying established property? You’re paying full stamp duty and getting no grant.

What Investment Buyers Are Seeing for Rental Returns

Gross rental yields by suburb:

- Barney Point: 6.11%

- South Gladstone: 5.58%

- Gladstone Central: 4.9%

- Regional average: 5.4%

Vacancy rate: 1.19% – meaning rental properties don’t sit empty. Tenant demand is strong.

Median weekly rent:

- Houses: $440-$470

- Units: $380-$425

Real investment scenario (South Gladstone):

- Purchase price: $475,000

- Required deposit (20%): $95,000

- Expected rental: $450/week ($23,400 annually)

- Gross yield: 5.58%

That’s solid by Australian standards. National average rental yields typically sit around 3-4%. Gladstone’s industrial employment base and tight housing supply create better returns.

How Long Getting Pre-Approval Actually Takes

Straightforward applications with local broker: 3-7 days

Your income is standard salary, you’ve got clean credit history, standard deposit from savings, buying a normal house. Pretty quick turnaround.

FIFO workers with proper documentation: 10-14 days

Takes longer because lenders need to verify your employment contract, understand your roster pattern, confirm income consistency across roster cycles. But it’s doable with a broker who knows how to document this properly.

Complex or non-conforming cases: 14-21 days with specialist lenders

Self-employed, previous credit issues, unusual property types – these need specialist lenders who take longer to assess but actually consider your full circumstances.

Direct bank applications: 14-30 days minimum

Going direct to banks without a broker? Expect longer timeframes. You’re dealing with call centres, generic assessment processes, and no one advocating for your specific situation.

When You Should Choose a Different Gladstone Broker

We promised transparency. Here are genuine scenarios where other brokers might suit you better.

Greg Hill Finance Suits You If…

You value working with the most established local name in town. That 196+ review volume on GetBirdEye provides confidence through sheer weight of feedback.

You need equipment finance for business operations – trucks, machinery, tools. Greg explicitly handles this alongside mortgages.

Standard business hours actually work for your schedule. You’re not doing shift work or FIFO, so 7am-7pm availability isn’t essential for you.

You prefer traditional broker office hours and established local presence over newer operations or extended service models.

Woods & Bauer Finance Suits You If…

You’re a small business owner who wants Andrew Bauer’s perspective as former BOQ Gladstone branch owner. That inside knowledge of how banks assess business lending is valuable.

You need servicing across both Gladstone and Brisbane. Their dual locations create convenience if you’re managing property in both cities.

You appreciate the energy of recently formed partnerships. Ryan and Andrew are bringing decades of individual experience into a fresh operation.

You have existing relationships with either Ryan or Andrew from their previous roles and trust their judgement.

Loan Market (Chris Maguire) Suits You If…

National franchise network backing matters to your confidence level. Being part of Loan Market’s 1000+ broker network provides institutional support.

Financial planning qualifications influence your decision. Chris holds both mortgage broking and financial planning diplomas.

You specifically value 10+ years of established director experience in the Gladstone area.

You want access to Loan Market’s proprietary systems, training, and support infrastructure.

Mortgage Choice (David Baker) Suits You If…

National brand recognition influences your comfort level. Mortgage Choice is Australia’s largest brokerage network.

You want the backing of REA Group ownership (since 2021) and award-winning brokerage credentials (The Adviser magazine’s #1 brokerage 2025).

You prefer established franchise systems and processes over independent operators.

Access to 40+ lenders through the Mortgage Choice panel meets your needs without requiring the broader 70+ lender access.

Gladstone Home Loans (Peter Miller) Suits You If…

You prefer independent local operators over franchises or newer partnerships.

Peter’s specific communication style and approach resonate with you based on initial conversations.

You value the existing client testimonials about straightforward advice.

You’re seeking a second opinion on advice you’ve already received elsewhere.

Different brokers genuinely suit different people. There’s no universal “best” broker – there’s the broker who fits YOUR specific situation, communication preferences, and priorities.

How to Actually Choose Between Gladstone Brokers

Stop reading Google reviews and star ratings for a minute. Here’s what actually matters.

Test Their Local Knowledge with Specific Questions

Ask about recent sales in specific streets. Ask why Barney Point is growing faster than West Gladstone. Ask how the renewable energy transition might affect property values over 10 years. Ask what happened to properties bought at the 2013-2014 peak during LNG construction.

Generic answers reveal imported expertise. Specific, nuanced responses demonstrate genuine local understanding.

Confirm Actual Lender Access, Not Marketing Claims

“We work with all major banks” could mean 4 lenders or 70 lenders. Ask specifically: How many lenders do you have on your panel? Do you have access to specialist non-conforming lenders? Can you handle low-doc or complex income situations?

Breadth matters, especially if your situation isn’t perfectly standard.

Match Operating Hours to Your Actual Schedule

If you’re working FIFO or rotating shifts, extended hours aren’t nice-to-have. They’re essential. Confirm when the broker is actually available, not just what their website claims.

Can you genuinely get appointments that work for your schedule? Or will you be taking unpaid leave to meet during business hours?

Verify Experience in Your Specific Situation Type

First-time buyer? Ask how many first-timers they’ve helped in the past 12 months. Investment property? How many investment loans have they settled recently? Self-employed? What documentation processes do they use?

General experience is fine. Specific experience in YOUR situation type is better.

For Complex Cases, Confirm They’ve Actually Placed Similar Applications

If your situation involves previous credit defaults, self-employment income, FIFO arrangements, or unusual property types, ask directly: Have you successfully placed applications similar to mine? Which lenders did you use? What documentation was required?

Brokers who say “we can definitely help” without specific examples might be optimistic rather than experienced.

Test Communication Style During Initial Consultation

Do they explain things clearly or use jargon? Do they listen to your situation or immediately jump to solutions? Do they ask good questions or just process information?

You’re going to be working with this person through a significant financial transaction. Communication compatibility matters.

Understand What Happens After Settlement

What ongoing service do they provide? Annual rate reviews? Proactive refinancing recommendations? Ongoing advice? Or do they disappear after settlement unless you contact them?

The relationship doesn’t end when your loan settles. Find out what post-settlement support actually looks like.

Clarify Fee Structure Upfront

Most Australian brokers earn lender commission rather than charging client fees. But confirm this explicitly. Are there any client fees? Application fees? Advice fees? Get clarity upfront.

No surprises after you’re already committed.

Read Actual Review Content, Not Just Star Counts

Don’t just count five-star reviews. Read what people actually say. What do they specifically praise? Do any complaints appear across multiple reviews? What patterns emerge?

Pay special attention to reviews mentioning situations similar to yours.

Value Independent Validation Over Marketing Claims

Industry awards are marketing. Reddit recommendations from property investors who researched multiple brokers? That’s genuine third-party validation from people with no incentive to promote anyone.

Look for evidence of brokers being recommended by actual clients with no commercial relationship.

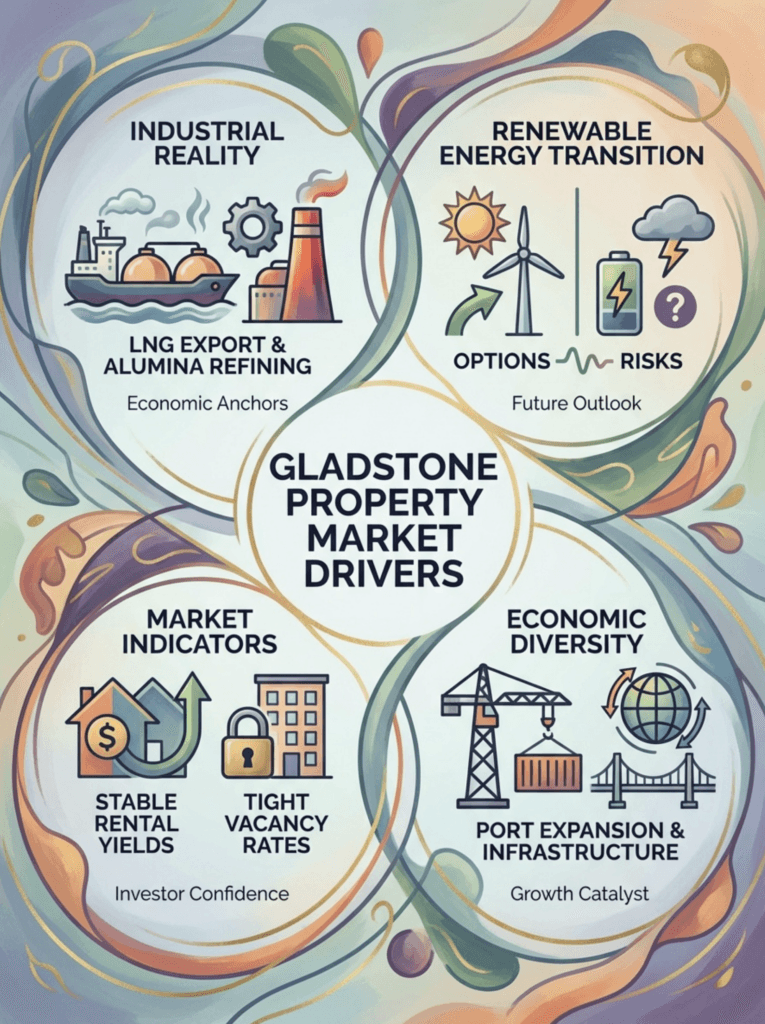

Understanding What’s Actually Driving Gladstone’s Property Market

You can’t make smart property decisions without understanding the economic foundation underneath.

The Industrial Reality

Gladstone’s economy centres on LNG export (three facilities – QCLNG, GLNG, Santos), alumina refining (QAL), port operations, and manufacturing. This industrial base provides employment stability but introduces economic cycles tied to commodity prices and industrial investment.

The property market experienced dramatic growth during LNG construction (2010-2016). Tradies were earning $200k+, rental properties were going for $800-$1200 per week, house prices were climbing 20-30% annually.

Then construction peaked. Employment dropped from roughly 10,000 construction workers to maybe 1,500 operational staff. Property prices crashed, dropping 30%+ in many suburbs. Rental vacancies spiked. People who bought at the peak lost serious equity.

Now we’re five years into recovery, with prices up 74% from those lows. But we’re still below the 2013-2014 peak in many areas.

Understanding this cycle matters. Are current growth rates sustainable? Or are we approaching another cycle peak?

The Renewable Energy Transition Creates Both Opportunity and Risk

Gladstone is positioning as a renewable energy hub. Hydrogen projects, industrial decarbonisation, renewable energy manufacturing. The 10-year economic transition roadmap aims to leverage existing industrial infrastructure for renewable production.

Success could drive long-term employment growth and property appreciation. Gladstone becomes Australia’s renewable energy manufacturing centre, attracting new industry and population.

Failure or slow transition could create employment challenges as traditional industries face carbon costs and international competition. LNG demand might decline as global markets shift toward renewables.

This transition risk doesn’t show up in current price data. But it’s worth considering for 10+ year property holds.

Why Rental Yields Stay Strong Despite Price Recovery

FIFO arrangements during construction drove rental prices to unsustainable levels. Workers were earning huge money and happy to pay $800/week for basic houses close to worksites.

When construction ended, rental prices crashed alongside property values. Landlords who’d bought at peak prices for peak rents got hammered on both sides.

Current rental yields (5.4% average) reflect more sustainable equilibrium. Strong industrial employment base, tight vacancy rates (1.19%), but without the construction premium inflating rents artificially.

The structural housing shortage supports these yields. Building approvals haven’t kept pace with population needs. That supply constraint maintains rental demand even as prices recover.

Infrastructure Investment Provides Employment Stability

Port expansion, industrial area development, renewable energy infrastructure – ongoing construction activity creates employment beyond pure industrial operations.

This matters for property because it provides economic diversity. You’re not purely dependent on LNG facility operational employment. Port expansion supports construction jobs, logistics employment, and service sector growth.

More economic diversity means less exposure to single industry cycles.

Making Your Final Decision

You’ve now got comprehensive information about Gladstone’s mortgage broking options, real market data you can verify, and honest assessments of different services.

Many Gladstone buyers choose AJ Home Loans based on extended 7am-7pm availability matching shift work reality, 20+ years local residency providing genuine market cycle understanding, unique money coaching supporting long-term success, first-time buyer specialisation with systematic processes, 70+ lender access creating genuine choice, specialist expertise for complex applications, and independent Reddit validation from property investors.

For situations involving complexity – FIFO income, previous credit challenges, self-employment, unusual properties, or previous bank declines – the 70+ lender panel access and specialist lending expertise become particularly valuable.

But make your own decision. Contact multiple brokers. Ask specific questions about your situation. Compare responses. Test communication styles. Choose the service that genuinely fits your needs.

If your situation is straightforward and you just need efficient processing, any competent broker can probably help you. If your situation involves complexity or you’ve already received declines, broader lender access and specialist expertise make a genuine difference.

Ready to Start?

Contact Coral Jacobs at AJ Home Loans Gladstone:

Phone: 0409 311 985

Address: 7/30 Tank Street, Gladstone Central

Website: ajhomeloansgladstone.com.au

Hours: 7am-7pm, seven days

Options: In-office, phone, or video consultations

Or contact the other brokers mentioned throughout this guide. Research properly. Choose wisely.

Your mortgage decision influences the next 25-30 years of your financial life. Taking time to make an informed choice is worthwhile.

Common Questions About Gladstone Mortgage Brokers

Who handles first-time buyers best in Gladstone?

AJ Home Loans specialises in first-timers with systematic processes for navigating the $30,000 First Home Owner Grant, stamp duty concessions, and lender credit assessment. The money coaching integration helps beyond just loan settlement. Multiple testimonials specifically mention patient, educational approach without pressure. The 7am-7pm availability works for shift workers who can’t access standard business hours.

What actually makes AJ Home Loans different from other Gladstone brokers?

Extended 7-day availability (7am-7pm), integrated money coaching, 20+ years Gladstone residency experiencing complete property cycles, first-time buyer specialisation, 70+ lender access including specialist non-conforming options, and willingness to handle complex cases other brokers decline. Only Gladstone broker offering financial literacy education alongside mortgage services.

How many lenders can AJ Home Loans actually access?

70+ lenders including major banks (NAB, ANZ, Westpac, CBA), regional banks, building societies, credit unions, and specialist non-conforming lenders. This compares to 40+ for Mortgage Choice and undisclosed panels for other local brokers. Broader access creates more options for complex situations that major banks automatically decline.

What hours does AJ Home Loans operate?

7am-7pm daily including weekends. Phone, video, or face-to-face appointments. This specifically serves FIFO workers and shift workers who finish night shift at 6am or start afternoon shift at 6pm. Every other Gladstone broker operates standard business hours.

Can they help if I’ve been declined by banks already?

Yes. The 70+ lender panel includes specialist non-conforming lenders who assess situations major banks automatically decline. Self-employed income, previous credit defaults, foreign income, low documentation scenarios, investment portfolios, unusual properties – situations where standard lending criteria don’t fit but genuine capacity exists. If you’ve received bank declines, broader lender access provides alternative pathways.

What are Gladstone house prices in 2026?

April 2025 data showed $526,328 median dwelling price with 22.6% year-over-year growth. Trending toward $570,000+ by mid-2026. Individual suburbs vary – Gladstone Central $550,000+, South Gladstone $475,000-$500,000. Rental yields range from 4.9% to 6.11% depending on location. Vacancy rate 1.19% indicates tight rental market.

How much is the Queensland First Home Owner Grant?

$30,000 for eligible first-time buyers purchasing or building new homes valued under $750,000. Extended to June 30, 2026. Combined with zero stamp duty on new builds (saving approximately $9,096), total government support reaches $39,096 for eligible buyers. Only applies to NEW homes, not established properties.

Does AJ Home Loans charge client fees?

Like most Australian mortgage brokers, income comes from lender commission rather than client fees. Any specific fees would be disclosed during initial consultation. Always confirm fee structure upfront with any broker you’re considering.