The essential takeaway: Lenders scrutinise spending habits to assess risk, while advertised interest rates are often negotiable starting points. Cleaning up bank statements three months prior and challenging the “loyalty penalty” by refinancing can secure approval and significantly lower payments. Notably, a mere 0.25% rate reduction saves over $28,000 on a $500,000 loan over 30 years.

Do you worry that your bank is quietly profiting from your loyalty while you struggle with rising interest rates and strict approval criteria?

This guide exposes exactly what mortgage lenders don’t want you to know about their hidden risk assessments and the discretionary pricing models that often disadvantage existing clients compared to new ones.

Uncovering these insider truths about application red flags and the real cost of fees will empower you to negotiate a better deal and avoid the expensive financial traps designed to maximize their profits at your expense.

- The Lender’s Microscope: What Your Bank Statements Really Reveal

- The Interest Rate Game: Why the Advertised Number Isn’t the Final Offer

- Application Landmines: The Small Mistakes That Cause Big Problems

- Beyond the Approval: The Long-Term Costs Lenders Don’t Advertise

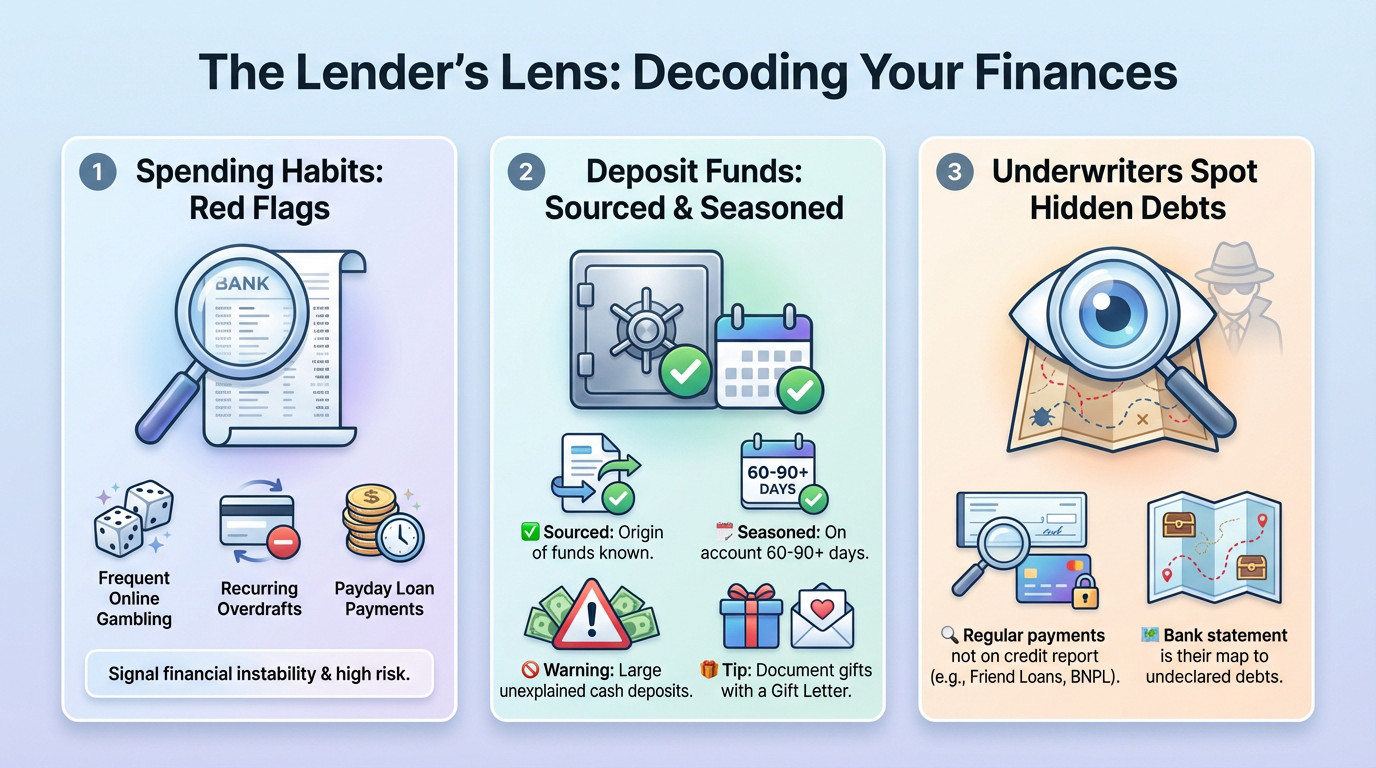

The Lender’s Microscope: What Your Bank Statements Really Reveal

You might think they just check your balance. Wrong. Lenders analyze your transactions to build a risk profile, and certain patterns make them very nervous.

The Story Your Spending Habits Tell

Lenders scour statements for red flags like frequent online gambling, overdrafts, or payments to payday loan services. These aren’t just hobbies to them; they signal deep financial instability and poor money management.

This isn’t a moral judgment on your lifestyle. To an underwriter, these habits suggest a high risk that paying your mortgage won’t be your top priority when money gets tight.

Even recurring payments they can’t identify look suspicious. They often view them as undisclosed debts, complicating your evaluation.

‘Sourced and Seasoned’: The Two Words That Matter for Your Deposit

Let’s define the terms. “Sourced” means the lender knows exactly where the money came from. “Seasoned” means it has sat in your account for a while, usually over 60 to 90 days.

Why does this matter? A large cash deposit right before you apply sets off alarm bells. The lender assumes it’s a hidden loan you’ll have to repay, which slashes your actual borrowing power.

If you receive a gift, document it. You need a proper gift letter to avoid the application crashing.

How Underwriters Spot Hidden Liabilities

Underwriters hunt for regular outgoing payments that don’t match debts on your credit report. This could be a personal loan to a mate or a “Buy Now, Pay Later” service.

Lenders aren’t just looking at the debts you declare; they’re hunting for the ones you don’t. Your bank statement is their map, and every recurring payment is a landmark.

Understand the difference between what a bank sees and how a broker prepares you

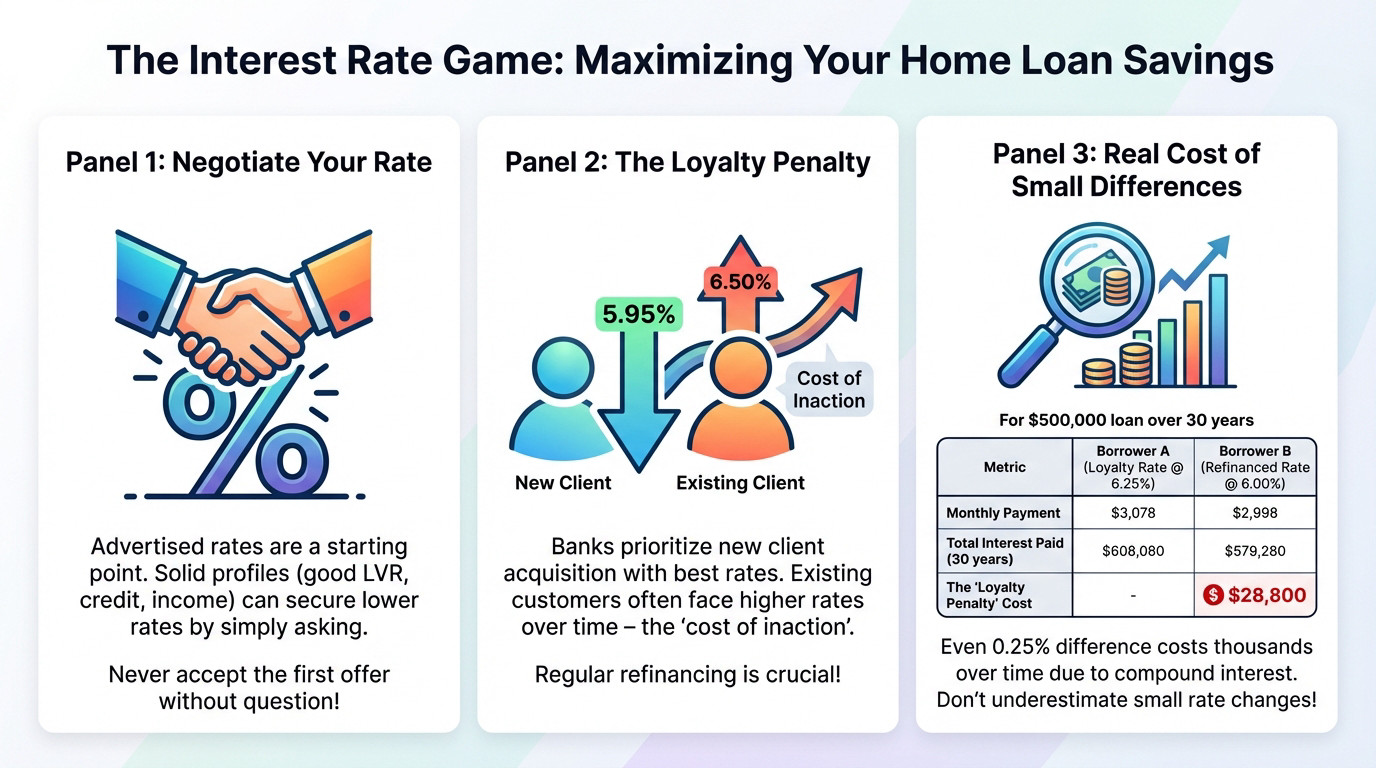

The Interest Rate Game: Why the Advertised Number Isn’t the Final Offer

Once your finances are scrutinized, the next hurdle is the interest rate. But the rate displayed in big print is rarely the one you should accept.

Discretionary Pricing: The Hidden Room for Negotiation

Most borrowers miss a key reality: lenders have wiggle room. The “advertised rate” is just a starting line for the general public. If you have a strong profile—solid LVR, stable income—you hold leverage to demand better.

Insiders call this “discretionary pricing.” Banks prefer shaving off points over losing a quality client to a competitor. So, never accept the first offer without asking.

The Loyalty Penalty: Why New Customers Often Get Better Deals

Sticking with one bank for decades rarely earns special treatment. Lenders pour their best rates into acquiring new customers, not rewarding faithful ones. Existing clients often face a “loyalty tax” where rates creep up quietly compared to the market.

This is why regular home loan refinancing is non-negotiable. Blind loyalty to a lender could cost you tens of thousands over your loan’s life in Gladstone.

How Small Rate Differences Create Huge Costs

A difference of 0.25% sounds negligible, doesn’t it? But over 30 years, that tiny fraction creates a massive gap. Compound interest works against you daily.

This is what mortgage lenders don’t want you to know: that “small” difference funds their profits, not your equity. Look at the real cost on a $500,000 loan.

| Metric | Borrower A (Loyalty Rate at 6.25%) | Borrower B (Refinanced Rate at 6.00%) |

|---|---|---|

| Monthly Payment | $3,078 | $2,998 |

| Total Interest Paid (30 years) | $608,080 | $579,280 |

| The ‘Loyalty Penalty’ Cost | – | $28,800 |

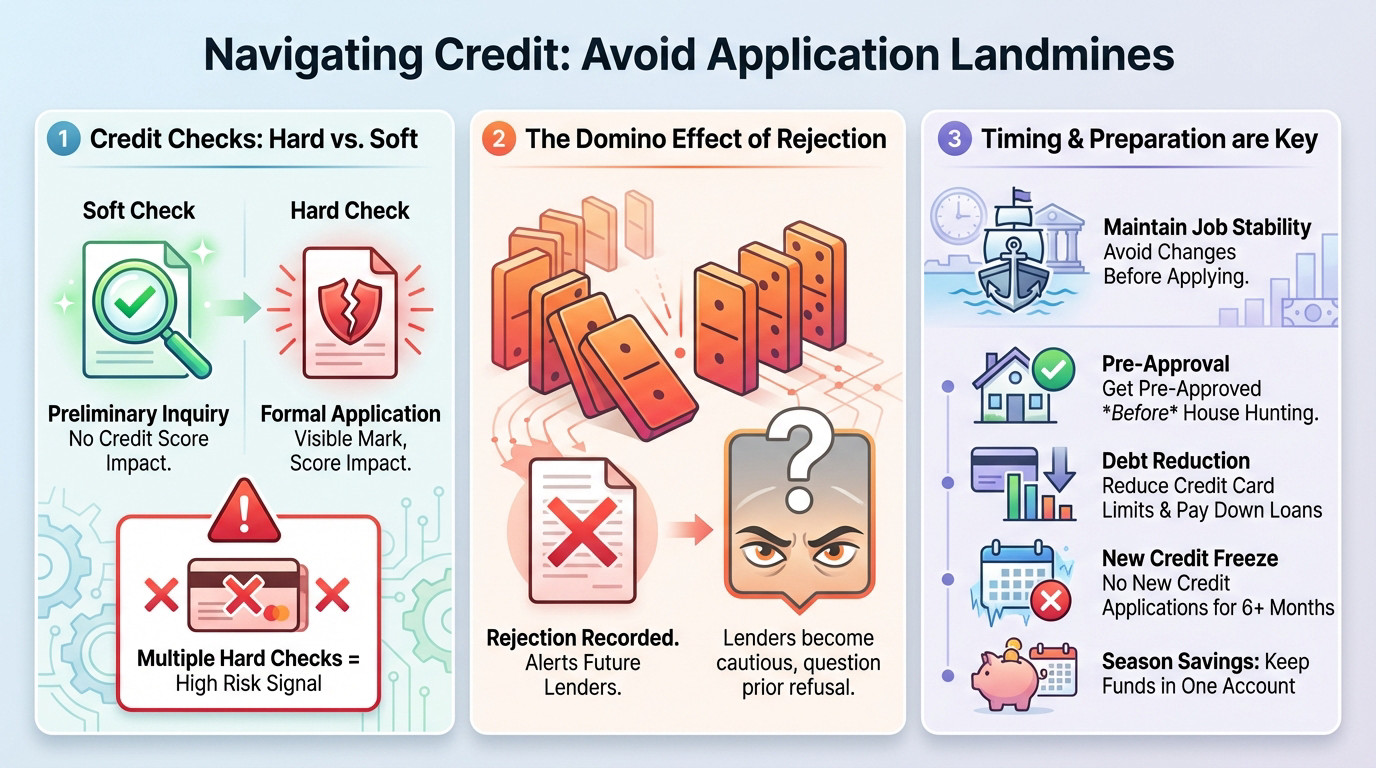

Application Landmines: The Small Mistakes That Cause Big Problems

Negotiating a rate is useless if you can’t get through the front door. You’d be surprised how many applications derail before a human even reviews them.

‘Hard’ vs ‘Soft’ Credit Checks: Shopping Around the Smart Way

A soft search is just a preliminary look at your file. It leaves no footprint on your credit score. A hard search, however, is a formal request for money. It leaves a visible mark that other lenders can see immediately.

The danger lies in racking up multiple hard searches quickly. It screams that you are desperate for credit, which instantly spikes your risk profile. Lenders hate desperation.

A smart broker uses soft searches to test the waters first. We check your eligibility without bruising your credit file.

The Domino Effect of a Rejected Application

When a bank says no, that rejection gets stamped on your history via the hard inquiry. The next lender sees it instantly. It’s a red flag they can’t ignore.

Even if the first bank rejected you for a minor policy reason, the second bank gets spooked. They immediately become more conservative. They wonder what the first lender saw that they haven’t found yet.

Why Timing and Preparation are Your Best Assets

Lenders crave stability above all else. Switching jobs or jumping into self-employment right before applying is a massive gamble. It often forces you to wait months to prove income reliability.

You need to scrub your finances clean before we submit anything. Here is how we prep your file for a yes:

- Get pre-approved before you start house hunting.

- Reduce your credit card limits and pay down personal loans.

- Avoid any new credit applications for at least six months.

- Keep your savings in the same account to ‘season’ them.

The market shifts constantly, and banks change their appetites for risk. While lending standards are evolving, preparation remains your best defense. Don’t let a timing error cost you the house.

Beyond the Approval: The Long-Term Costs Lenders Don’t Advertise

Getting approval is just the starting line. This is exactly what mortgage lenders don’t want you to know: the decisions you make now, often based on incomplete info, dictate your loan’s true cost for decades.

Your Borrowing Capacity Is a Limit, Not a Target

Lenders calculate your maximum capacity using basic models to protect their risk, not your comfort. This figure completely ignores your actual lifestyle or specific savings goals.

Borrowing the full amount leaves you “house poor,” where every cent vanishes into the loan. You lose the financial wiggle room needed when life happens.

A savvy borrower sets a budget well below the lender’s limit. This buffer protects you from the risk of ending up with an ‘underwater’ mortgage.

The Critical Difference Between an Offset and a Redraw Facility

An offset is a separate transaction account linked directly to your loan. The balance reduces interest daily, but crucially, the money remains yours to control completely.

A redraw facility means you have paid extra directly onto the loan principal. To access it, you must request to “withdraw” funds, which lenders can sometimes restrict.

An offset offers genuine flexibility and safety. A redraw can be risky if you need those funds urgently.

Fees That Quietly Drain Your Finances

Lenders rely on hidden fees to boost profit margins. You face application costs, annual fees, and expensive “break costs” that accumulate quickly.

The interest rate gets your attention, but the fees are where the real long-term damage is done. A low-rate loan with high fees can easily be more expensive over time.

- Common Fees to Watch For

- Application/Establishment Fees (upfront cost).

- Ongoing Annual/Monthly Package Fees.

- Discharge/Settlement Fees (when you leave).

- Break Costs (for exiting a fixed rate early).

Mastering the lender’s playbook transforms you from a passive applicant into a powerful negotiator. By spotting hidden costs and challenging the “loyalty penalty,” you secure your financial future rather than just a loan approval. Ready to find the right deal? Book an appointment in Gladstone today to discuss your options.

FAQ

Do lenders really look at my individual daily transactions?

Yes, they absolutely do. Lenders scrutinise your bank statements to build a risk profile that goes far beyond just checking your account balance. They are specifically hunting for “red flags” such as frequent gambling transactions, regular overdraft usage, or payments to payday loan services, which suggest financial instability.

This is not a moral judgement, but a calculation of risk. If an underwriter sees patterns indicating that loan repayments might not be your top priority, or spots recurring payments to undeclared debts, it can jeopardise your application regardless of your income level.

Can I negotiate the interest rate displayed on the bank’s website?

The advertised rate is rarely the final offer. Lenders often use “discretionary pricing,” which gives them the flexibility to offer lower rates to borrowers with strong profiles, such as a high credit score or a low Loan-to-Value Ratio (LVR).

Banks rely on the fact that most customers accept the first number they see. By simply asking for a better rate or presenting a competitor’s offer, you can often secure a discount that saves you thousands of dollars over the life of the loan.

Why do I need to explain where my deposit money came from?

Lenders require your funds to be “sourced and seasoned” to prevent fraud and ensure you haven’t secretly borrowed the money for your deposit. “Sourced” means proving the origin of the funds, while “seasoned” typically means the money has been sitting in your account for at least 60 to 90 days.

A large, unexplained cash deposit just before you apply is a major warning sign for underwriters. To avoid delays, ensure any large transfers or gifts are fully documented with a clear paper trail well before you submit your application.

Will shopping around for a mortgage damage my credit score?

It depends on how the checks are performed. A ““soft check” is a preliminary review that does not impact your credit file, whereas a full application triggers a “hard check”. Too many hard checks in a short period can make you look desperate for credit.

However, credit scoring models usually treat multiple hard enquiries for a mortgage within a 45-day window as a single event. This allows you to compare offers from different lenders without ruining your credit score, provided you do it within that specific timeframe.

Is an offset account better than a redraw facility?

While both options reduce the interest you pay, an offset account generally offers more control and safety. An offset is a separate transaction account linked to your mortgage; the money remains yours and is easily accessible if you need it for emergencies.

A redraw facility, by contrast, involves paying extra directly into the loan principal. While you can often “redraw” this extra money, the lender may have the right to refuse or limit access to these funds if your financial situation changes, making it a riskier place to store your emergency savings.