If you’ve ever wondered why your friend or relative with a similar income got approved while you didn’t—or why your application sailed through when you expected drama—you’re not alone.

The home loan approval process feels like a black box to most people. You submit your application, cross your fingers, and wait. But here’s the thing: lenders aren’t making random decisions. They’re following specific criteria, and understanding what they’re actually looking for can be the difference between approval and rejection.

I’m Coral Jacobs from AJ Home Loans Gladstone, and I’ve spent years helping locals navigate the home loan maze. I’ve seen applications that looked impossible get approved, and seemingly straightforward cases hit unexpected roadblocks.

Let me pull back the curtain and show you exactly what lenders scrutinise—with real examples from right here in Gladstone.

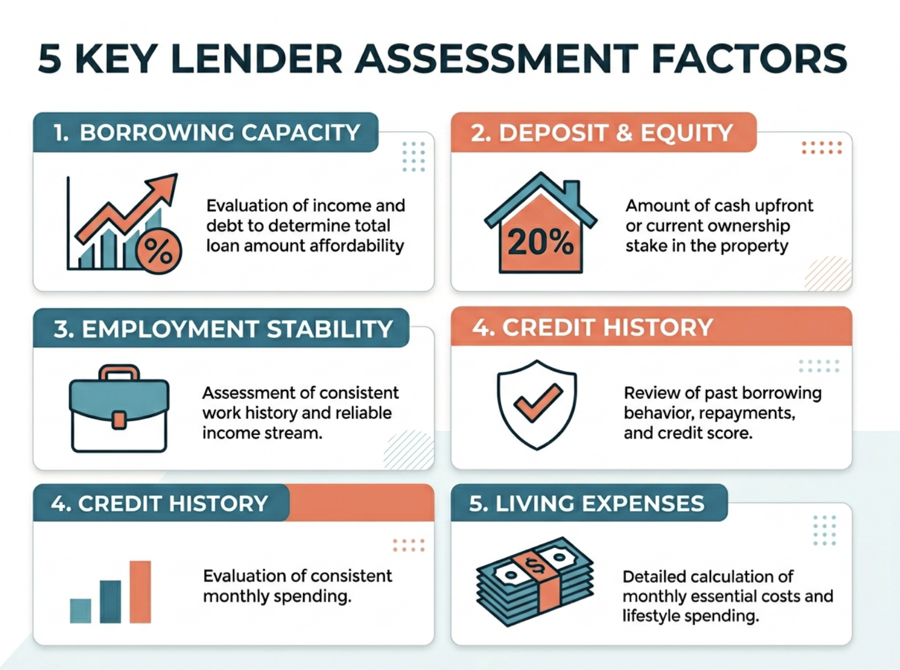

The 5 Factors Every Lender Obsesses Over

When a lender assesses your application, they’re not just ticking boxes. They’re building a picture of you as a borrower. Here’s what they’re really examining:

1. Borrowing Capacity and Serviceability

This isn’t just “can you afford the repayments?” It’s “can you afford them when rates go up?” Lenders stress-test your application at rates 2.5–3% higher than the actual loan rate. If you’re looking at a 6% interest rate, they’re calculating whether you could handle 8.5–9%.

2. Deposit and Equity Position

The magic number is 20%. Hit that deposit threshold and you avoid Lenders Mortgage Insurance (LMI), open up more lender options, and strengthen your application significantly. But don’t despair if you’re below that—it’s absolutely possible to get approved with less.

3. Employment Stability and Income Type

Lenders love stable, ongoing PAYG employment. Self-employed, casual, and contract workers can absolutely get approved, but expect stricter documentation requirements. The key phrase lenders look for? “Long-term in the role.”

4. Credit History and Conduct

Here’s a surprise: it’s not just about your credit score. Lenders examine how you’ve managed existing debts. Missed payments, defaults, or too many recent credit enquiries raise red flags—even if your score looks decent.

5. Living Expenses and Financial Behaviour

Since the Banking Royal Commission, lenders scrutinise bank statements like forensic accountants. Your spending habits, existing debts, and lifestyle expenses all factor in. That means your Saturday night pokies habit or collection of buy-now-pay-later accounts could cost you thousands in borrowing power.

Real Gladstone Clients: What Got Them Approved

Let me share some real scenarios I’ve worked on. Names changed, obviously, but these situations will probably sound familiar.

The First Home Buyer Couple

Both worked full-time PAYG jobs with a combined income around $135,000. They had 5% deposit—funds gifted from family plus the First Home Owner Grant. They purchased a $400,000 property.

What made it work? Stable employment, a letter confirming the gift was genuine (not a loan in disguise), clean bank statements, and zero debt. The consistent savings pattern, even though small, showed lenders they could manage money responsibly.

The Single Parent

Single income earner, PAYG full-time, bringing in around $80,000. Small deposit, used a family guarantee to avoid LMI. Purchased a $330,000 property.

The winning factors? A consistent savings pattern despite being a single income household, stable employment history, genuine savings, and—crucially—they paid out all existing debts before applying. That debt clearance boosted their borrowing capacity significantly.

The Self-Employed Tradie

Sole trader pulling $100,000 on tax returns, 10% deposit, purchasing around $425,000.

Here’s what worked: Two years of tax returns and financials (lenders need to see consistent self-employed income), genuine savings for the deposit, and—this is key—we found a lender that assessed his income favourably. Not all lenders treat self-employed income equally, and that’s where broker expertise matters.

The Refinance That Saved $8,000 a Year

Existing homeowner who hadn’t reviewed their loan in six years. They were on a rate nearly 2% higher than current market rates.

The result? Refinanced their loan and saved significant money annually. What made it work was good equity position, clean repayment history, and comparing multiple lenders to find the best deal. This one’s a reminder: if you haven’t reviewed your loan in over two years, you’re probably paying too much.

When Things Don’t Go to Plan: Real Rejection Stories

Not every application gets approved, and understanding why can save you months of frustration.

The Unknown Credit Default

Client walked in confident, ready to buy. Then we pulled their credit report and found a default they had no idea existed—an old phone bill from a previous address that went to collections without them receiving notice.

The major banks declined automatically. The client was genuinely shocked.

How we fixed it: First, we verified whether it was legitimate or an error. If it’s an error, we dispute it with the credit reporting agency. If it’s real but paid, we find lenders willing to look past it based on overall conduct. If it’s outstanding, we help pay it out and place the client with a specialist lender who assesses applications on merit rather than automated scoring.

The Job Change That Killed the Deal

This catches people constantly. A client landed a better-paying job and thought it would strengthen their application. Wrong.

Even moving from one diesel mechanic role to another—same industry, better pay—can cause issues. Some lenders want probation completed (3–6 months). Others just need one payslip. But some won’t proceed at all until you’ve proven yourself in the new role.

Worse scenario? Going from PAYG to self-employed, like a tradie going out on their own. Suddenly you’re treated as self-employed, which typically requires 1–2 years of tax returns. Your old PAYG income can’t be used, your new self-employed income isn’t established—you’re in a gap where neither income counts.

The trap? Most first home buyer grants require mainstream lending, which means that 2-year self-employed history. Without the grant, you’re looking at higher rates, higher fees, and likely paying LMI because your deposit is smaller.

The Property That Didn’t Stack Up

Client was approved from an income and credit perspective, but the property valuation came in $25,000 below the purchase price.

Resolution? We helped renegotiate the purchase price and increased the deposit to cover the shortfall. Sometimes the issue isn’t you—it’s the property.

How Lenders Really Treat Different Types of Income

Not all income is equal in lenders’ eyes. Understanding this can save you significant heartache.

- PAYG (Full-Time/Part-Time): The gold standard. Lenders accept 100% of base salary. They prefer 2 years in the same employment type—gaps or industry changes complicate things.

- Self-Employed: Minimum 2 years trading history with full tax returns and financials. Some lenders consider 1 year. Specialist low-doc options exist but come with higher rates.

- Casual Employment: At least 12 months in the same role with consistent hours. Some lenders are flexible, others aren’t.

- Overtime and Bonuses: Usually accepted at 80%, with 2-year history required to prove consistency.

- Rental Income: Lenders shade this by 20–30%, meaning they’ll only count 70–80% of gross rent to account for vacancies and expenses.

The Deal Breakers Nobody Expects

These catch people off guard constantly:

- Too Many Lending Accounts: It’s not one Afterpay account—it’s Afterpay plus Zip plus Humm plus Klarna. They all add up and each one generates a credit enquiry.

- Shopping for Credit Before Applying: That car loan you applied for three months ago? Still on your credit file. Those five BNPL accounts you signed up for? Five enquiries.

- Spending Habits: Excessive gambling transactions, frequent cash withdrawals, or regular betting account transfers are major red flags.

- Guaranteeing Someone Else’s Loan: That full debt counts against your borrowing capacity.

Gladstone-Specific Factors You Need to Know

Our local economy creates unique considerations:

Contract and FIFO/DIDO Workers: Common in Gladstone due to Rio Tinto, Gladstone Ports Corporation, and LNG projects. Some lenders love this income type, others are nervous about it.

Regional Property Valuations: Lenders can be conservative with regional area valuations. Some have postcode restrictions that limit LVR. Interestingly, even properties within the same postcode get treated differently depending on specific location and property type.

Your 60-Day Approval Action Plan

Want to improve your chances? Here’s what actually works:

- Clean Up Bank Statements: Cut unnecessary subscriptions, avoid gambling, demonstrate consistent savings. Lenders review 90 days of statements.

- Pay Down or Close Unused Credit: That $10,000 credit card with zero balance? Still reduces your borrowing power because lenders assess the full limit.

- Avoid New Credit Applications: No car finance, credit cards, or personal loans. Every enquiry shows on your file.

- Get Documents Organized: Payslips, tax returns, bank statements, ID—all in your name, showing current address.

- Talk to a Broker Early: Get your position reviewed before formally applying. Avoid surprises and wasted credit enquiries.

The Broker Advantage: Why It Matters

Here’s the reality: different lenders have wildly different appetites for different scenarios. One bank’s automatic decline is another lender’s easy approval.

Major banks typically have the sharpest rates but the strictest criteria. Non-bank lenders and specialist lenders are often more flexible with self-employed income, credit history, and non-standard scenarios.

As a broker, I have access to a wide panel of lenders and can compare options to find the best fit for each client’s unique situation. Just because one lender says no doesn’t mean they all will—and that’s exactly where broker expertise adds real value.

The Bottom Line

Getting approved for a home loan in Gladstone isn’t about luck or knowing the right people. It’s about understanding what lenders actually assess and positioning your application accordingly.

Whether you’re a first home buyer, self-employed, working FIFO, or looking to refinance, there’s a path forward. Sometimes it’s straightforward. Sometimes it requires strategy, timing, and finding the right lender.

The key? Don’t go in blind. Talk to someone who knows the local market, understands lender criteria, and can give you a realistic picture of where you stand.

Ready to find out where you stand? Get in touch with AJ Home Loans Gladstone for a no-obligation chat about your situation. We’ll review your position, identify any issues, and give you a clear action plan—before you waste time and credit enquiries on applications that won’t fly.