Essential takeaway: A deposit represents only the entry fee, not the final cost. True financial safety requires budgeting for substantial upfront charges like stamp duty and LMI, alongside ongoing liabilities such as council rates and the recommended 1% annual maintenance fund. Anticipating these hidden layers prevents post-settlement shock and preserves critical emergency savings.

Saving for a deposit often feels like the hardest part, but missing the hidden home buying costs Australia throws at you can quickly turn your property dream into a sudden financial nightmare. We break down every unexpected fee lurking beyond the sale price, including government charges and insurance, to ensure your hard-earned savings survive the transaction.

Discover the complete expense checklist you need to budget for today so you can secure your keys without facing a single nasty surprise.

- The Upfront Costs That Hit Before You Get the Keys

- The Financing Costs That Catch Most Buyers Out

- The Settlement and Moving Day Costs That Drain Your Savings

- The Ongoing Reality: Budgeting for Ownership, Not Just a Mortgage

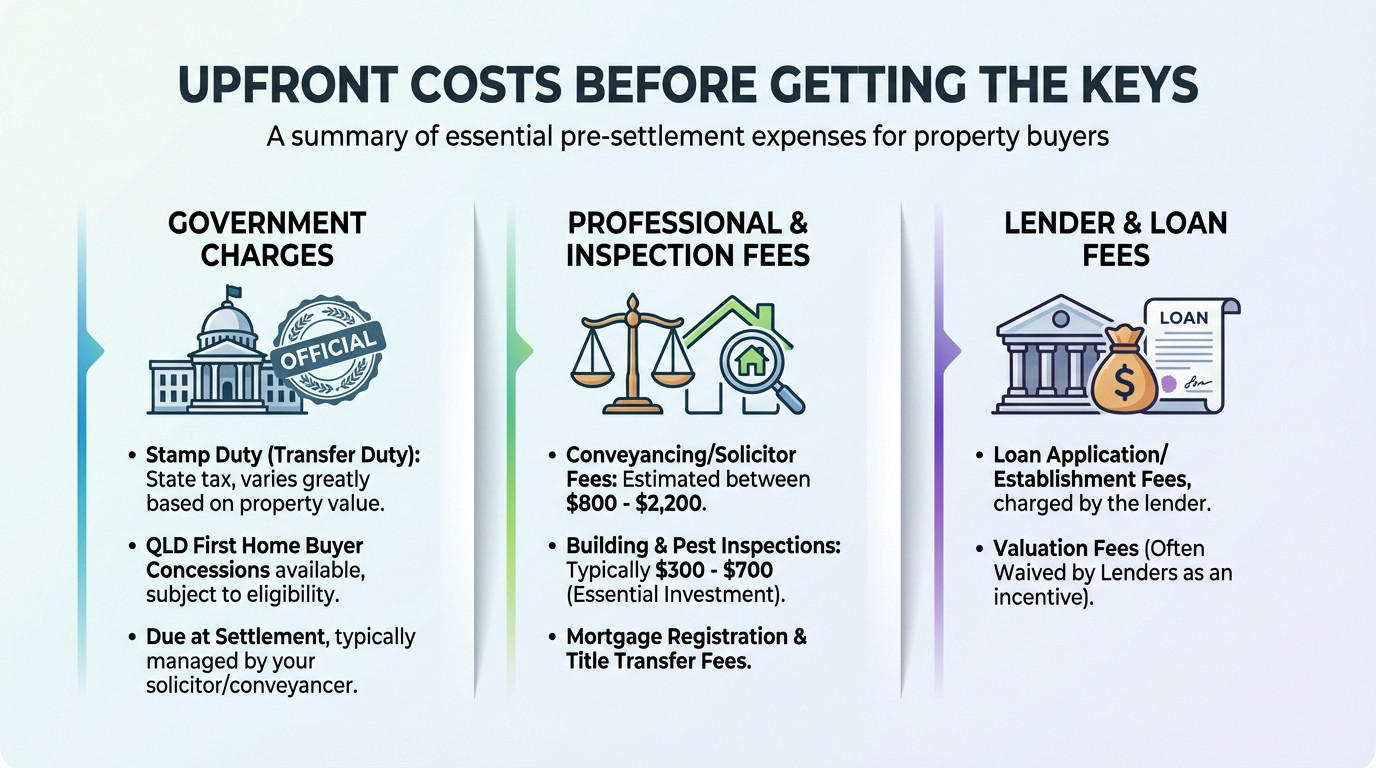

The Upfront Costs That Hit Before You Get the Keys

Most buyers obsess over the deposit, thinking it’s the only hurdle. But the real financial shock comes from the expenses that land on your desk weeks before you ever touch the front door handle. These are the costs that can drain your bank account if you aren’t prepared.

Government Charges You Can’t Ignore

Let’s talk about transfer duty, often called stamp duty. It is essentially a hefty state tax levied on your property purchase. The exact amount you pay fluctuates significantly based on the property’s value.

Here in Queensland, the news is better for newbies. You might qualify for first home concessions that drastically slice or even eliminate this bill. It hinges on the purchase price and living there, so check the Queensland Government site.

You must budget for this immediately because this bill lands right at settlement.

Essential Professional Fees for Your Protection

You need a conveyancer or solicitor to handle the legal heavy lifting. They ensure the property legally becomes yours without nasty surprises. Expect to pay roughly $800 to $2,200 for this service.

Never skip building and pest inspections. Think of this as insurance against buying a money pit, not just another expense. Spending $300 to $700 now saves you from thousands in hidden termite damage later.

Don’t forget mortgage registration and title transfer fees. These are mandatory government administrative costs you simply cannot dodge.

The Lender Fees to Get Your Loan Started

Banks often charge a loan application or establishment fee just to set up your mortgage. It covers their administrative costs for processing your paperwork and getting the account ready.

Then there is the valuation fee. The lender orders this to confirm the property is actually worth what you are paying. While you usually foot the bill, some lenders might waive this cost to win your business.

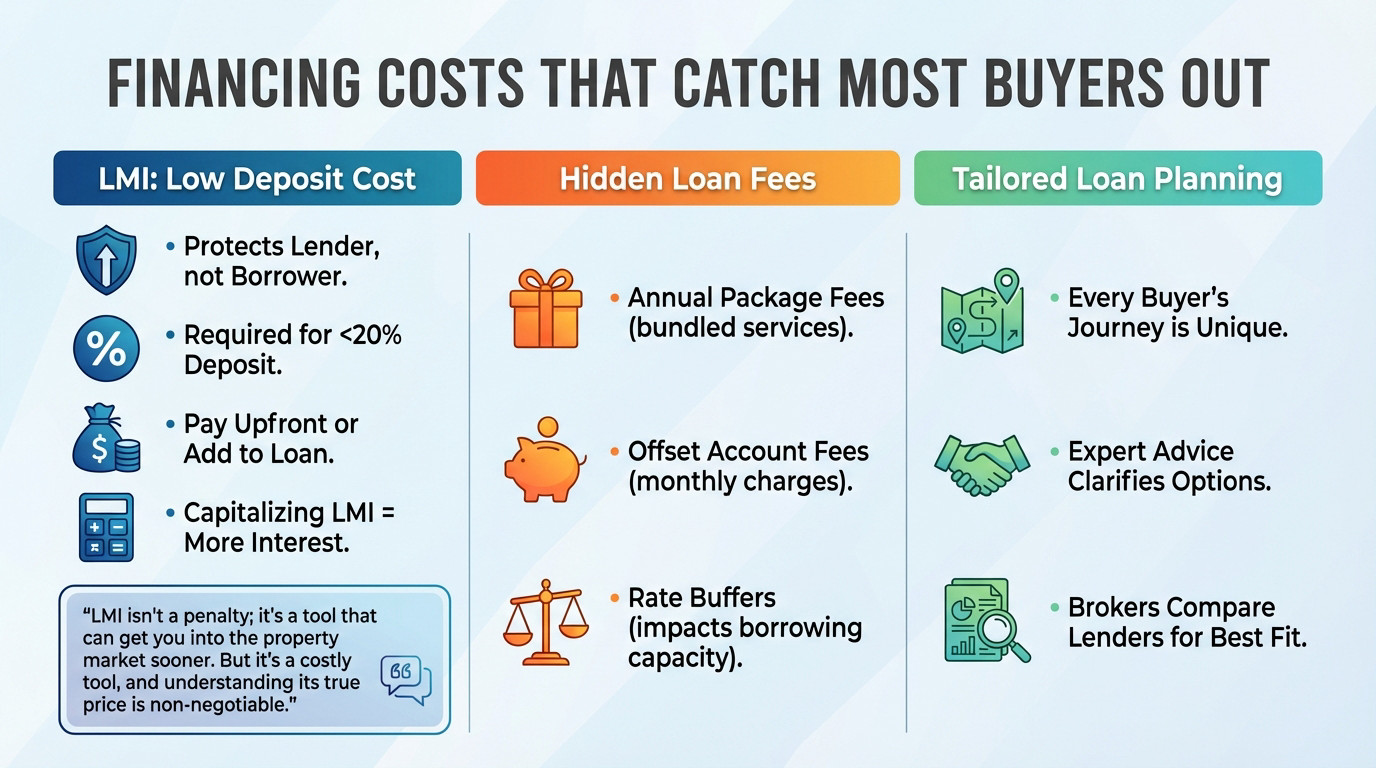

The Financing Costs That Catch Most Buyers Out

Now that the upfront fees are clear, let’s look at the financing itself. This is where the biggest financial shocks hide, especially if you’re working with a smaller deposit.

Lenders Mortgage Insurance (LMI): The Price of a Low Deposit

Lenders Mortgage Insurance (LMI) is often misunderstood. It protects the bank, not you, in case you default. You will generally face this cost if your deposit sits below 20% of the property’s purchase price.

You have two choices for payment. You can pay the premium upfront at settlement, or you can “capitalise” it by adding the amount to your total loan balance.

Be careful with capitalisation. Since it increases your loan size, you pay interest on that insurance premium for the next 30 years, costing you thousands more.

LMI isn’t a penalty; it’s a tool that can get you into the property market sooner. But it’s a costly tool, and understanding its true price is non-negotiable.

Understanding Your Loan Structure and Its Hidden Fees

Watch out for annual package fees. Lenders often bundle your mortgage with a credit card or other products, charging a yearly fee that eats into your budget silently.

Offset accounts can also sting. If an offset isn’t included in a package, banks often charge a monthly service fee just to keep that account open.

Then there are rate buffers. Banks test your ability to repay at 3% higher than your actual rate, which significantly reduces your borrowing power.

Planning for Your Specific Loan Type

Every buyer’s financial situation is different. Navigating these costs requires a strategy tailored to you. We help you explore specialised first home buyer loans that fit your specific needs and long-term goals.

A broker helps you compare products across different lenders. We find the structure that minimizes these hidden home buying costs Australia throws at you, separating the big banks’ offers from smarter alternatives.

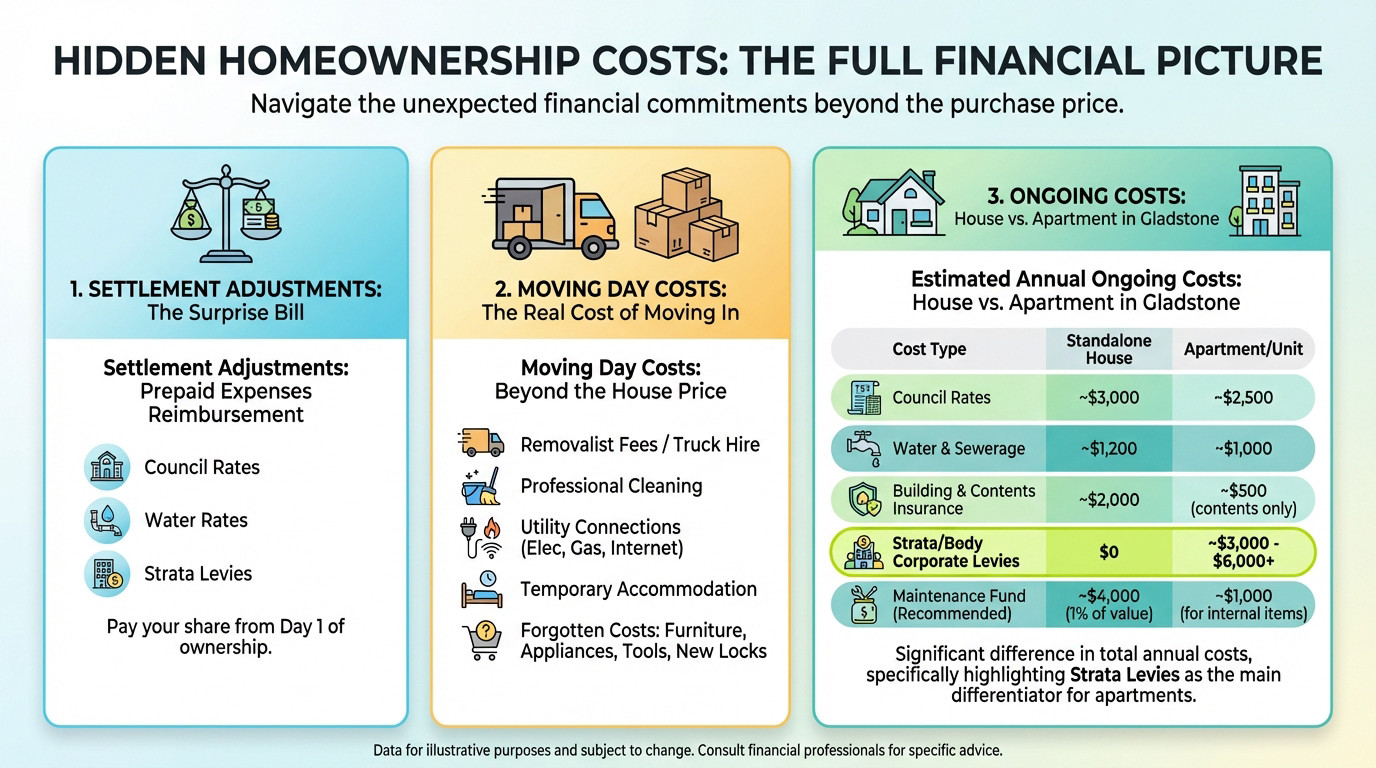

The Settlement and Moving Day Costs That Drain Your Savings

Finance is approved and you finally have a settlement date. But the cash outflow doesn’t stop there. The hidden home buying costs Australia residents face right before and after keys are handed over are the ones that typically empty bank accounts.

The Surprise Bill: Settlement Adjustments

Settlement adjustments are often a nasty shock for new buyers. This is simply the process where you reimburse the vendor for specific property bills they have already paid in advance.

You will face pro-rata charges for council rates, water rates, and for apartments, the strata levies. You are responsible for paying your share starting strictly from the day you become the legal owner.

The Real Cost of Moving In

People budget for the house price but frequently forget to budget for the logistical nightmare of moving.

- Removalist fees or truck hire

- Professional cleaning costs (for your old rental and maybe the new place)

- Utility connection fees (electricity, gas, internet)

- Temporary accommodation if there’s an overlap

Don’t ignore the silent wallet-drainers like new furniture, appliances that don’t fit the fridge cavity, and first-week “essentials” like a lawnmower, basic tools, or new locks.

Ongoing Costs: Apartment vs. House in Gladstone

Ongoing ownership costs vary significantly depending on whether you secured a standalone block or a strata-titled unit.

| Cost Type | Standalone House (Example) | Apartment/Unit (Example) |

|---|---|---|

| Council Rates | ~$3,000 | ~$2,500 |

| Water & Sewerage | ~$1,200 | ~$1,000 |

| Building & Contents Insurance | ~$2,000 | ~$500 (contents only) |

| Strata/Body Corporate Levies | $0 | ~$3,000 – $6,000+ |

| Maintenance Fund (Recommended) | ~$4,000 (1% of value) | ~$1,000 (for internal items) |

| Total | ~$10,200 | ~$8,000 – $11,000+ |

The Ongoing Reality: Budgeting for Ownership, Not Just a Mortgage

Once you are settled, the invoices start landing in the letterbox. Real financial discipline actually kicks in after moving day, and that’s where a solid budget separates comfort from panic.

Your New Regular Bills Are Not Optional

You now own the mandatory recurring costs: council rates, water charges, and home and contents insurance. Most lenders won’t even settle the loan unless you prove that insurance policy is active.

These bills often hit quarterly or annually, easily totaling thousands of dollars. I always tell clients to stash cash in a separate offset account weekly so you aren’t scrambling when they arrive.

The Most Forgotten Cost: Maintenance and Your Cash Buffer

You need a dedicated maintenance fund. A smart rule of thumb involves setting aside about 1% of your property’s value every single year just for upkeep and repairs.

Think about a hot water system blowing up, a sudden roof leak, or a storm-damaged fence. These are no longer a landlord’s headache; they are solely your problem.

This is why you shouldn’t drain every cent for the deposit. Keeping a cash buffer is your only real safety net against debt when life happens.

The real financial stress of home ownership isn’t the monthly mortgage payment. It’s the unexpected $5,000 repair bill when your savings account is at zero.

Avoiding the Stress: How to Prepare Properly

Preparation beats panic every time. Sitting down with a mortgage broker in Gladstone helps you build a realistic budget that factors in every single one of these costs, not just the loan repayments.

Understanding these expenses upfront lets you make decisions based on facts, not guesswork. It stops you from falling into the common mistakes first home buyers make, ensuring you buy your home with total confidence.

- Your First Home Buyer Cost Checklist

- Stamp Duty & Government Fees

- Legal & Inspection Fees

- Lender & LMI Costs

- Settlement Adjustments (Rates, Water)

- Moving & Connection Fees

- Ongoing Ownership Costs (Insurance, Strata)

- A dedicated cash buffer (3-6 months of expenses)

Buying a home involves more than just the deposit. Understanding these hidden costs ensures you are financially prepared for the reality of ownership.

Don’t let surprise bills derail your property journey. Contact AJ Home Loans Gladstone today to build a realistic budget and secure your first home with confidence.

FAQ

How does stamp duty work for first home buyers in Queensland?

Stamp duty (also known as transfer duty) is a state government tax charged on property transactions, and it is often the largest upfront cost outside of your deposit. However, Queensland offers specific concessions for first home buyers. Currently, if you purchase an established home valued under $500,000 to live in, you may be eligible to pay zero stamp duty.

For properties valued between $500,000 and $550,000, a sliding scale concession applies, reducing the amount you pay compared to a standard investor. It is vital to budget for this early, as stamp duty is payable at or before settlement and cannot usually be added to your home loan.

What is Lenders Mortgage Insurance (LMI) and does it protect me?

A common misconception is that Lenders Mortgage Insurance protects the borrower; in reality, it protects the lender in the event that you default on your loan and the property is sold for less than the debt owed. You are generally required to pay for this insurance if your deposit is less than 20% of the property’s purchase price.

While LMI is an additional cost, it can be a useful tool to help you enter the property market sooner without saving a full 20% deposit. Many lenders allow you to “capitalise” this fee, meaning it is added to your total loan amount and paid off over time with your mortgage, rather than requiring an upfront cash payment.

What are settlement adjustments and why do I have to pay them?

Settlement adjustments are calculations performed by your solicitor or conveyancer to ensure ongoing property costs are split fairly between the seller and the buyer. If the seller has already paid council rates, water access charges, or body corporate fees for the current quarter, you must reimburse them for the period where you will own the property.

These adjustments are added to the final amount you need to provide on settlement day. Because these figures vary based on the specific handover date and the billing cycles of local councils (like Gladstone Regional Council), it is smart to keep a cash buffer of roughly $500 to $2,000 to cover these surprise additions.

Do I really need to pay for building and pest inspections?

Yes, paying for professional building and pest inspections is essential for your financial protection. While it may feel like an extra $300 to $700 expense, these reports can reveal structural defects, termite activity, or moisture issues that are invisible to the untrained eye.

Consider this fee an investment rather than a cost. If the inspection uncovers major issues, you can often use the report to negotiate a lower purchase price to cover repairs, or you can withdraw from the contract entirely, saving you from buying a “money pit” that could drain your savings for years.

Are the ongoing costs higher for a house or an apartment in Gladstone?

The ongoing costs vary significantly between property types. With a standalone house, your main ongoing costs are council rates, water, and your own building insurance. You also need to manage a personal “sinking fund” for maintenance, but you have control over when repairs are done.

For apartments or units, you will typically pay Body Corporate (strata) levies. These are mandatory quarterly fees that cover building insurance and common area maintenance. While you might not have to mow the lawn yourself, these fees can be substantial—often thousands of dollars a year—and must be paid regardless of your personal financial situation.